Contributed by: Angela Palacios, CFP®, AIF®

Investors with the patience to hold on to their diversified portfolio that maintains a component of international have likely been rewarded this year. Before this year, investors challenged the advice of diversifying their portfolio away from the U.S. as international investments, represented by the MSCI EAFE, noticeably lagged U.S. returns in recent years. The chart below shows how the MSCI EAFE has performed vs. the S&P 500. When the gray shaded area is above 0, this represents a time when the prior three years of returns have been dominated by the MSCI EAFE outperforming the S&P 500. When you drill down into specific extended time periods when this happens, you can see that much of the returns come from the impact of the currency return (the lighter green portion of the return). You see in recent years the S&P 500 has significantly outperformed international investments.

A weakness in the U.S. dollar has contributed to the outperformance year-to-date by the MSCI EAFE (as of 9/30/2017 the MSCI EAFE was up XX% vs. the S&P 500 was up XX%). When the dollar is in a cycle of weakening against foreign currencies, there is a natural tailwind helping performance. Coupled with the global economy strengthening and political risks receding due to a failed populist movement in Europe, this could be a continuing recipe for international investing tailwinds.

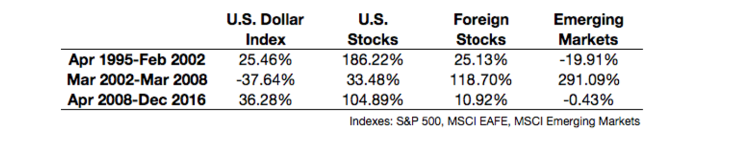

Take a look at the impact on stock markets around the globe during these periods of different U.S. dollar trends:

When the U.S. dollar index is retreating, Foreign and Emerging markets have outperformed and vice versa. If the U.S. dollar continues its current trend of weakening or even levels out, we could continue to see the performance story dominated by foreign investments.

Angela Palacios, CFP®, AIF® is the Director of Investments at Center for Financial Planning, Inc.® Angela specializes in Investment and Macro economic research. She is a frequent contributor The Center blog.

This information has been obtained from sources deemed to be reliable but its accuracy and completeness cannot be guaranteed. This information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Opinions expressed are those of Angela Palacios and are not necessarily those of Raymond James. There is no assurance the trends mentioned will continue or the forecasts provided will prove to be correct. Investing involves risk, investors may incur a profit or loss regardless of the strategy or strategies employed. International investing involves special risks, including currency fluctuations, differing financial accounting standards, and possible political and economic volatility. Investing in emerging markets can be riskier than investing in well-established foreign markets. The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. stock market. The MSCI EAFE (Europe, Australasia, and Far East) is a free float-adjusted market capitalization index that is designed to measure developed market equity performance, excluding the United States & Canada. The EAFE consists of the country indices of 21 developed nations. The MSCI Emerging Markets is designed to measure equity market performance in 25 emerging market indices. The index's three largest industries are materials, energy, and banks. Please note direct investment in an index is not possible. Index performance does not include transaction costs or other fees, which will affect actual investment performance. Individual investor's results will vary. Past performance does not guarantee future results.