Contributed by: Robert Ingram, CFP®

Contributed by: Robert Ingram, CFP®

Non-qualified stock options (NQSOs) are a form of employer compensation that gives an employee the right to purchase a specific number of company shares at a predetermined price within a defined time period. Unlike direct stock grants Restricted Stock Units (RSUs), which provide actual shares of stock, NQSOs offer the option, but not the obligation, to buy shares in the future.

If you have access to these stock options, they can be one of the most valuable opportunities to build wealth through your employer—but they are also frequently misunderstood. On the surface, it might seem straightforward: you can buy your company’s stock at a set price and benefit from future growth. In practice, stock options involve a series of decisions that can have financial and tax consequences that unfold over time. From grant and vesting to exercise and eventual sale, each stage in the lifecycle of these NQSOs carries its own rules and implications for the value you ultimately realize.

Grant: It Starts with a Promise (Not Ownership)

When your company grants you stock options, you don’t actually receive stock. You receive something much more subtle: the right to buy stock later at a fixed price.

You’re told:

How many options you have (number of shares you could buy)

At what price you’ll be able to buy them (exercise price)

When you’ll be allowed to use that right (the vesting schedule)

And when the opportunity expires

As a hypothetical example, let’s say you were granted 4,000 options on May 1st, 2026, with an exercise price of $20 per share. The vesting schedule is that 25% of the total options vest after one year, and the remaining 75% of the options vest quarterly over the next three years. Finally, the expiration date is May 1st, 2036 (10 years from the grant date). Whoa! There’s a lot there. Let’s tackle it in stages.

At this stage, nothing has happened financially. No cash or value is exchanged. There are no actionable steps, and there is no taxation. There is just the potential opportunity that begins when your options vest.

Vesting: You Earn the Right to Act

Over time, those options that were granted “vest.” This means that the options become exercisable. The option becomes “yours,” and you can choose to exercise (or not exercise) the options (i.e., purchase shares with some or all of the vested options).

In most employee stock option plans, vesting is gradual, often spread out over a few years.

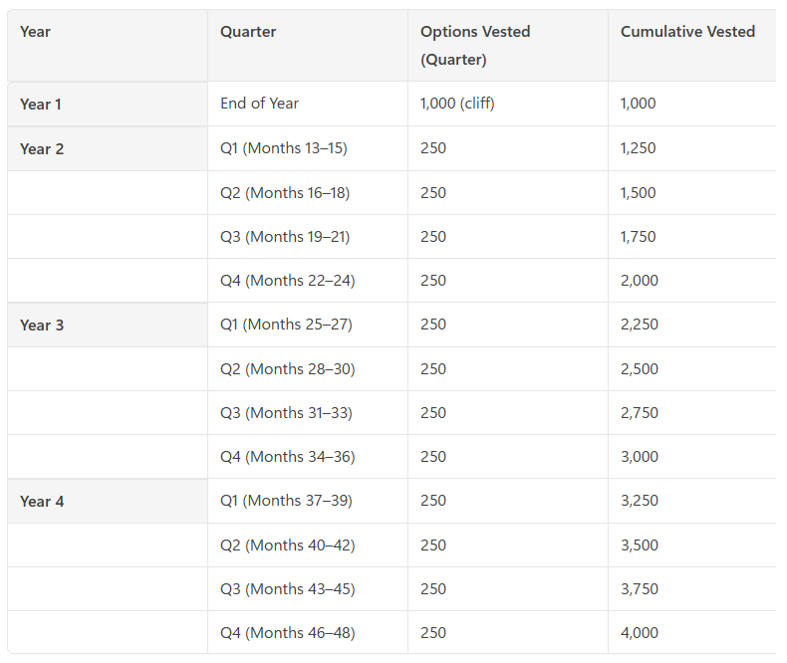

In our example above, the first 1,000 options vest one year from the grant date, so they would be exercisable on May 1st, 2027. From there, portions of the unvested shares vest each quarter for the next three years.

The following table illustrates how a vesting schedule might look, where each quarter an equal number of options vest from the end of year 1 until the end of year 4.

While this is a common type of vesting schedule, it is very important to understand your own employer’s specific vesting plan and to know when your options will be available to exercise. Until the options vest, they are not truly “yours,” and you may forfeit any future right to exercise them if you leave the employer, for example.

But here’s a key point about each vesting date: at vesting, still nothing happens financially. Vesting does not trigger taxes.

This is different from other types of equity compensation, such as Restricted Stock Units (RSUs). When RSUs vest and you receive shares, the total value of the shares at that time is considered income and would be reported and taxed as ordinary income.

When non-qualified stock options vest, there is still no action taken, and you haven’t received the value of any options, so there is no reported income or associated taxes. But now, your planning and decision-making start.

Exercising: When You Buy—and Taxes Kick In

Eventually, you reach the first decision point: do you exercise your options?

The value of stock options comes from the difference between what you’re allowed to pay for the stock and what it’s actually worth in the market.

So, from our example, let’s say you have options that have vested, and the value of the stock in the market is $45 per share. Because your options have an exercise price of $20 and you could purchase shares for $20, there is a gain of $25 per share ($45 - $20). The options allow you the opportunity to build that value without having to buy the shares outright (yet!).

Now, when you do exercise options (i.e., buy the shares) at any time up until the expiration date, this is where things change and taxes come into play.

At the time you exercise, the difference between the market value of the shares and the price you are able to pay to buy them is considered income and is reported to the IRS. In our example, if the value at the time of exercise is $45 per share and your purchase price is $20, you would have ordinary income of $25 per share.

If you exercised 1,000 shares, that would be 1,000 × $25 → $25,000 in taxable income.

Many people assume taxes happen when they sell the shares. While sales can and often do occur around the same time as the exercise, the exercise itself often triggers the biggest tax impact.

If you choose to exercise options in a high-income year, the extra income may push you into higher tax brackets. Another scenario is waiting to exercise large groups of options all at once. This could also dramatically change your overall income in that year and therefore impact your tax liability. This is why careful tax planning is an important part of managing your stock options.

Quick Note on Taxes at Exercise (and How They’re Paid)

Taxes here aren’t just reported and owed—they’re typically withheld. Employers are generally required to withhold taxes at the time of exercise. This usually includes federal taxes, state income tax, Social Security, and Medicare (FICA taxes). How is the withholding paid?

Methods for covering taxes:

Cash payment (out of pocket) – sending payment from your bank or wire transfer to cover the taxes

Selling shares to cover – the plan sells a portion of exercised shares to cover the taxes

This is the most common approach used

Withholding shares – the plan withholds a number of shares equal in value to the taxes instead of selling shares on the market

This is less common for public company stock option plans

Selling Shares: Turning the Value into Cash

To fully realize the usable value of the options and shares, you would sell the shares for cash as the final financial outcome and decision.

Taxes may come into play again after you exercise and sell your shares (as capital gains or losses).

Remember, at exercise, the difference between the market value and the exercise price is already taxed as income, so the cost basis of the exercised shares becomes the market value at the time of exercise.

Cost basis in our example: if exercising shares when market value was $45 → cost basis = $45

If you were to sell those shares for $55, for example → you would have a $10 capital gain.

If, on the other hand, you sold the shares at $35 → you would have a $10 capital loss.

Depending on when you choose to sell your exercised shares, you could have a short-term capital gain or loss (if held for less than one year) or a long-term capital gain or loss (if held for more than one year). With the tax treatment differences between short-term and long-term capital gains, this again adds further tax planning considerations to your decisions.

Note: You are typically responsible for any taxes associated with these capital gains or losses, as they are not withheld by the employer plan.

From Exercise to Ownership to Selling: (How You Get There)

When you exercise your options, you’re no longer holding an option—you now own stock. There is generally no maximum holding period before having to sell, and there is no risk of losing rights to the shares if you leave the employer, retire, etc.

But there are a few methods for exercising options and turning them into real value.

Pay in cash (hold all shares) – covering the cost of the share purchases and usually the tax withholding by writing a check or transferring funds to the plan administrator. You retain all of the shares until you decide to sell some or all of them.

At this point, you might be asking, “What if I don’t have the cash, or I don’t want to use my funds to exercise the options?”

Cashless Exercise:

Sell some shares at exercise (hold some shares) – a portion of shares is sold immediately to cover the cost of the shares exercised (and usually the tax withholding). You retain the remaining shares.

You would then hold the remaining shares for investment until you decide to sell them.

The other type of cashless exercise is one of the most common methods for using options and converting them into usable value:

Cashless exercise (sell everything) – you exercise options, and all the shares are sold immediately, covering the cost of shares and taxes, leaving you with cash proceeds instead of stock.

This full cashless exercise allows you to turn the value of your options into cash in one step with no out-of-pocket cost and avoids the ongoing risk of holding the stock. That can be very advantageous for many people.

However, there may be cases where exercising options to hold shares makes sense. One advantage is that potential future growth may be taxed at capital gains rates, which could be lower than ordinary income rates. Depending on your current income and expected future income, this difference may significantly impact your overall outcome.

Bottom Line

Stock options are more than just a one-time benefit. They involve a process and decisions based on many factors over several years (even a decade or longer). Small differences in timing, taxes, and personal choices at each step add up to shape your results.

As with many complex financial decisions that have tax and other implications, you should consult with your financial planner and tax advisor.

If you’ve received stock options and aren’t completely confident in how they fit into your overall plan, we’re happy to have a conversation.

Please don’t hesitate to contact us!

Robert Ingram, CFP®, is a CERTIFIED FINANCIAL PLANNER™ professional at Center for Financial Planning, Inc.® With more than 15 years of industry experience, he is a trusted source for local media outlets and frequent contributor to The Center’s “Money Centered” blog.

Securities offered through Raymond James Financial Services, Inc., member FINRA/SIPC. Investment advisory services are offered through Center for Financial Planning, Inc. Center for Financial Planning, Inc. is not a registered broker/dealer and is independent of Raymond James Financial Services.

The foregoing information has been obtained from sources considered to be reliable, but we do not guarantee that it is accurate or complete. Any opinions are those of Bob Ingram, CFP® and are not necessarily those of RJFS or Raymond James. Raymond James Financial Services, Inc. and its advisors do not provide advice on tax issues, these matters should be discussed with the appropriate professional.