Timothy Wyman, CFP®, JD: Tim was quoted in Forbes on September 6, 2012 in an article titled; "Jumping Out The 401(k) Brokerage Window" by Ashlea Ebeling. This story appears in the September 24, 2012 issue of Forbes. Click here to read the entire article.

Timothy Wyman, CFP®, JD: Tim was quoted in Forbes on September 6, 2012 in an article titled; "Jumping Out The 401(k) Brokerage Window" by Ashlea Ebeling. This story appears in the September 24, 2012 issue of Forbes. Click here to read the entire article.

Open Enrollment: Health Insurance and Medicare Enrollment

Reviewing health care insurance options is as important as getting a physical or flossing (and about as much fun). For employees age 65 and older, this decision becomes more complicated due to Medicare eligibility. Major questions arise for this group of employees:

Reviewing health care insurance options is as important as getting a physical or flossing (and about as much fun). For employees age 65 and older, this decision becomes more complicated due to Medicare eligibility. Major questions arise for this group of employees:

- What, if any, health insurance coverage will my employer provide when I turn 65?

- Should I apply for Medicare at age 65?

- If I apply for Medicare, what parts should I apply for (A, B, D)?

Legally, employers can drop employees from their group health plans once they turn 65. But Medicare secondary payer rules prevent employers from reducing health benefits to current employees due to their eligibility for Medicare (except for very small employers). So, the employer must offer equal health benefits to all employees; coordinating health benefits with Medicare is allowed as part of this offering.

Employers with more than 20 employees typically offer group health coverage to 65+ employees, with Medicare acting as the secondary payer. In this case, eligible employees should enroll in Medicare Part A, hospital coverage, which is free. These employees should also get a deferral from Medicare so that they are not subject to penalties for enrolling in Parts B and D in the future.

Employers with less than 20 employees offer group coverage that is the secondary to Medicare. In this case, eligible employees should enroll in Medicare Parts A and B (Part B covers medical services, including doctor visits). Failing to enroll in both parts of Medicare could leave them responsible for paying out-of-pocket for anything that Medicare would have covered.

Here are some tips and considerations for employees age 65+ in making health insurance and Medicare enrollment decisions:

✔ Coordinate with your spouse. If you are both still working at age 65, you can compare employer health plans and how they work with Medicare. If spousal/family coverage is available, choose the optimal plan.

✔ Get in writing the details of your employer-provided coverage to help you decide how to handle Medicare choices.

✔ Plan to enroll in Medicare Part A (it’s free!) up to 3 months prior to your 65th birthday. You can sign up online or at your local Social Security office.

✔ If you are planning to enroll in Medicare Part B or Part D (prescription drug coverage), you can enroll up to 3 months prior to age 65 or within 8 months of retirement or loss of group health coverage (if you miss the 8 month Special Enrollment Period, you will need to wait until the next General Enrollment Period for that coverage).

✔ Consult with a CERTIFIED FINANCIAL PLANNER™ to help you choose the benefits that are most appropriate for your financial situation.

✔ Most importantly, do your research and plan ahead; Medicare has strict enrollment periods and rules that come with financially penalties.

This is the third blog in our 8-part open enrollment series. Check back in the upcoming days for more important tips to help you make the best choices for the upcoming year.

Sandra D. Adams, CFP® is a Lead Financial Planner at the Center for Financial Planning, Inc. In 2012, she was named to the Five Star Wealth Managers list in Detroit Hour magazine. In addition to her frequent contributions to Money Centered blogs, she is a regularly quoted in national media publications such as the Wall Street Journal, Research Magazine and the Journal of Financial Planning. Sandy is a frequent speaker on the topic of Elder Care Financial Planning.

Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Any opinions are those of Center for Financial Planning and not necessarily those of RJFS or Raymond James.

Open Enrollment: Health Insurance

At this time of year, many of you might have an opportunity to select a medical plan as part of your employer’s open enrollment period. Selecting the appropriate medical plan is one of the most important decisions each year. We all have heard stories, unfortunate stories, of hard working folks that have significant financial issues due to extreme medical expenses. This blog post isn’t written to convince anyone that they need adequate health insurance – rather it is meant to provide some thoughts and tips on how to make the best choice for you and your family.

At this time of year, many of you might have an opportunity to select a medical plan as part of your employer’s open enrollment period. Selecting the appropriate medical plan is one of the most important decisions each year. We all have heard stories, unfortunate stories, of hard working folks that have significant financial issues due to extreme medical expenses. This blog post isn’t written to convince anyone that they need adequate health insurance – rather it is meant to provide some thoughts and tips on how to make the best choice for you and your family.

Employers that offer multiple medical plan options generally offer three types:

- Traditional

- Preferred Provider Organization (PPO)

- Health Maintenance Organization (HMO).

Traditional: This option usually provides the greatest flexibility in accessing doctors and hospitals. And, as you might expect, usually carries the highest monthly premium, deductible, and copay on services.

PPO: This option provides for lower premiums and copays as compared to the traditional plans if you visit doctors and hospitals within the PPO network. There is some flexibility in that you can seek services out of the network if desired, albeit at a higher cost in terms of deductible and/or copayment.

HMO: The HMO option generally features the lowest cost in terms of monthly premiums, deductibles and copayments in exchange for less flexibility. Each person must select a primary care physician whom is responsible for directing your overall care.

Here are some more tips and considerations in selecting medical insurance during open enrollment period:

✔ Coordinate with your spouse: It may make sense to both be covered by one employer’s plan depending upon your premium sharing requirements.

✔ New children: Sometimes the plan that was appropriate for a couple is no longer the best plan with kids. If your family is growing, consider a plan with a lower doctor visit copayment.

✔ High(er) deductible plan: These can be great options as they reduce your monthly premiums in return for potentially higher deductibles. Be sure that you have adequate cash reserves.

This is the second blog in our 8-part open enrollment series. Check back in the upcoming days for more important tips to help you make the best choices for the upcoming year.

Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Any opinions are those of Center for Financial Planning and not necessarily those of RJFS or Raymond James.

We're Sorry, This Page is No Longer Available

Checkout our current blog posts HERE. See you there!

Euro 101: Scandals

What does the country of Greece have in common with companies like Enron, WorldCom and Tyco International? The answer: Accounting scandals of epic proportions!

What does the country of Greece have in common with companies like Enron, WorldCom and Tyco International? The answer: Accounting scandals of epic proportions!

History Lesson 4

In 1992 the creation of the Maastricht Treaty required all members of the Eurozone to limit their Deficit spending and total debt levels in relation to their Gross Domestic Product (GDP), laying the groundwork for later establishment of the Euro as a common currency. The parameters for Government finance are:

- The yearly deficit that the individual country runs may not exceed 3% of the annual GDP of the country. Exceptions to this must be approved.

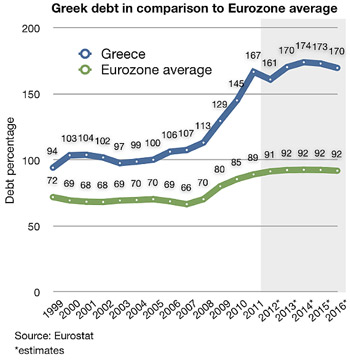

- Government Debt as a percent of GDP must not exceed 60%; however, there are only a couple of Eurozone countries that meet this criteria now. As a whole the Eurozone countries average over 90% as shown in the chart below.

Because of these requirements, countries like Greece (who far exceeds the 60 % acceptable level at 161% Debt to GDP) and Italy got more creative with their accounting methods and ignored internationally agreed upon standards in order to stay part of the Eurozone and use the Euro as their currency. Leaders masked their deficit and debt levels through a combination of techniques, including inconsistent accounting, off-balance-sheet transactions (like leaving out large military expenditures or billions in hospital debt) as well as the use of complex currency and credit derivatives structures.

Two years ago Greece had to fess up to these lies because they were unable to repay their debt. There was a loss of confidence prompting the rescue by other Eurozone countries, as they were the holders of much of this debt, and the International Monetary Fund.

This brings us to where we are today and one of the major questions the world is debating... ”Whether or not the Euro will survive”. I will discuss some of these opposing viewpoints in the next and final installment of this series.

Source: Spiegel Online International

Link to:

Lesson 1: A Little History Behind the Euro Zone Crisis

Lesson 2: Who’s in the Euro Zone and Why Was It Established?

Lesson 3: The Beginning of the End

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Any opinions are those of Center for Financial Planning, Inc., and not necessarily those of RJFS or Raymond James.

Center Included in 2012 Crain's List Largest Money Managers

The Center has been recognized among the top 25 largest money managers in Crain's Detroit Business. To view the Crain's List, please click on image below.

The Center has been recognized among the top 25 largest money managers in Crain's Detroit Business. To view the Crain's List, please click on image below.

Click here to view the profile of Timothy W. Wyman, CFP®, JD.

When Should You Take Social Security?

Baby boomers, on average, are living longer than any previous generation. While that’s good news, it also presents new challenges.

Baby boomers, on average, are living longer than any previous generation. While that’s good news, it also presents new challenges.

-

1) A longer life increases the likelihood that you’ll have increased medical and long-term care expenses.

2) The value of your nest egg will be more significantly impacted by increases in the cost of living over a longer term

When you consider these factors, it’s more important than ever to make calculated decisions about when to begin drawing Social Security benefits within the context of your overall retirement income plan.

According to the Social Security Administration, 74% of retired Americans drawing retirement benefits are receiving permanently reduced amounts. Reduced benefits are the result of filing when you first become eligible for benefits at age 62. Social Security rules are built around full retirement age (FRA), which is the age at which you are entitled to your full retirement benefit or Primary Insurance Amount (PIA).

The reason the PIA is an important number to know is because it is the base amount on which:

• Reductions will be made

• Increases given or

• On which spousal benefits are determined

Eligible Americans who turn 62 this year must wait until age 66 to begin receiving full payments. But they can receive smaller payments beginning as soon as age 62, or larger lifetime payments beginning as late as age 70. The net effect of filing at age 62 will be a 25% permanent reduction of annual benefits. On the other hand, those waiting until age 70 will see their benefit bumped up by 8% for every year they wait to file from age 66 to age 70. That’s a permanent 132% increase in benefit amount for life!

Here is a hypothetical example illustrating how the math works:

If Boomer Betsy decides to apply at age 62, or waits until FRA of 66, or delays to age 70. Boomer Betsy’s PIA is $2,230.

Age 62: Benefit amount is permanently reduced by 25% from $2230 to $1672

Age 66: Full retirement age benefit of $2230

Age 70: Benefit increases 8% per year from age 66 to 70 increasing from $2230 to $2943

Of course, there’s no telling how many years you will be collecting benefits but with careful planning, a strategy can be developed to improve potential lifetime benefits of Social Security by structuring the benefits to begin at optimal times based on your financial plan.

Have a social security question? Send me an email.

Click Here to get information on our upcoming seminar on Social Security Planning.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Any opinions are those of Center for Financial Planning, Inc., and not necessarily those of RJFS or Raymond James.

Tim Wyman Attends Leadership Oakland Class of XXIII

Tim Wyman, CFP® recently began participation in Leadership Oakland - just as Laurie Renchik, CFP® did one year ago. The program is intended to help selected participants (about 50 per year) learn about Oakland County, our region and state in order to be informed contributors within our communities.

Tim Wyman, CFP® recently began participation in Leadership Oakland - just as Laurie Renchik, CFP® did one year ago. The program is intended to help selected participants (about 50 per year) learn about Oakland County, our region and state in order to be informed contributors within our communities.

Tim recently attended a 2.5 day Retreat with 50 of his newest friends. He traveled to Roscommon Michigan to the R. A. MacMullan Conference Center. The group spent their time getting to know more about Oakland County, each other, and themselves and their leadership potential. The rustic camp setting provided a great learning and relationship building container. Although Tim commented that the bunk houses made college dorm rooms look spacious!

Tim and the other participants will engage in future sessions including; Economy & Government, Human services & Non Profits, Health & Environment, Diversity & Inclusion, Justice System, Education, Arts & Culture, Shaping the Future, and finally a class project.

We're Sorry, This Page is No Longer Available

Checkout our current blog posts HERE. See you there!

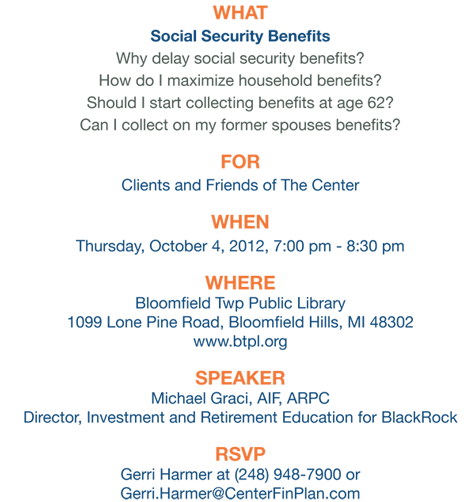

You're Invited: Maximize Social Security Benefits