Contributed by: Angela Palacios, CFP®

While many of us, including me, are eager for the new season of Game of Thrones to begin to see what happens next in Westeros, another game is surfacing around our world. Countries around the world are changing the rules of the game by pushing interest rates into negative territory. What happens when this occurs? Winter seems to be inevitable for the citizens in the seven kingdoms but is it inevitable for us?

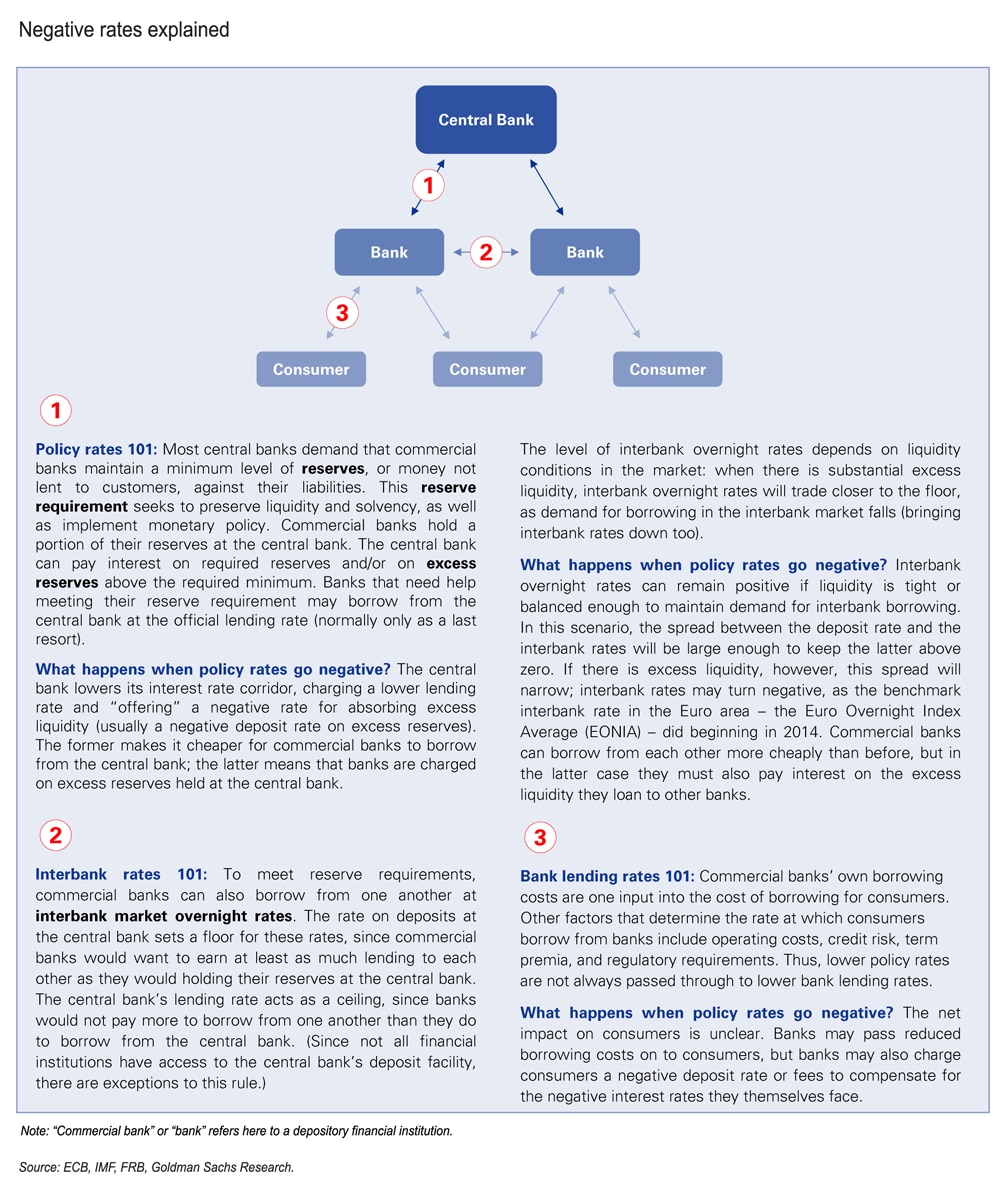

My colleague Nick Boguth recently wrote a blog explaining the different types of interest rates: Policy, Interbank, and Bank lending rates. Each of the rates is affected differently when interest rates are pushed into negative territory but all are ultimately connected.

When Policy Rates go Negative

This is the money paid to banks when they deposit their excess reserves with the Central Bank or have to borrow from the Central Bank to meet their reserve requirements. When these rates go negative it makes it cheaper for commercial banks to borrow to meet their reserve requirements but can actually cost the bank money when they park their excess reserves with the Central Bank overnight. Like the Iron Bank of Braavos “The Iron (Central) Bank will have its due.” This encourages banks to look around for something else to do with their excess reserves, like looking to each other to borrow from and lend to rather than the Central Bank.

When Interbank Rates go Negative

Banks lending to each other is affected by negative rates as they must now pay to lend money to another bank. The only way they would do this is if they had to pay less to loan their money to another bank than to pay to park it at the Central Bank. Neither of these situations is desirable. Institutions desire to earn money on these excess reserves rather than pay to loan to anyone. That has spurred them to buy short-term government debt with their excess reserves to try to seek some yield and the result is that they have pushed Government yields in certain countries, like Germany, into negative territory too. This, in turn, also drags down rates on corporate debt as they are correlated to government bond yields.

When Bank Lending Rates go Negative

The domino effect of all of these negative rates should pass through to the consumer but doesn’t always show up in lending rates. This negative deposit rate pushes down rates on short-term loans of other types of lending the bank does, like home and auto financing. But other factors, such as credit risk (while a Lannister always pays their debts, consumers don’t) and term premia can put a floor on how low rates can go to the consumer. Favorable lending rates also can be made up with charging consumers more to park their money in the bank. In theory, this downward pressure on rates is supposed to provide an economic boost while also weakening the country’s currency.

No one knows how the series Game of Thrones is going to end as the books have yet to be written. Like the show, the book has not yet been written on the full impact of negative interest rates either. It remains to be seen how this game ultimately ends!

{kind=link}

This material is being provided for information purposes only. Any opinions are those of Angela Palacios and not necessarily those of Raymond James. The information has been obtained from sources considered to be reliable, but Raymond James does not guarantee that the foregoing material is accurate or complete.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users and/or members.