Contributed by: Mallory Hunt

Contributed by: Mallory Hunt

"The key to making money in stocks is not to get scared out of them." – Peter Lynch

When it comes to investing, the phrase "stay the course" is practically gospel. It's repeated in market downturns, shared in financial blogs (this may currently resonate…), and printed on motivational coffee mugs. And rightly so—emotional decisions are one of the biggest threats to long-term investment success. While staying the course is a powerful mindset for long-term investors, it can often be seen as a call for inaction, and you very well may be sick of hearing the phrase, but it's not inaccurate. Just like a plane on autopilot still needs a pilot in the cockpit, your portfolio still needs your eyes—just not your panic.

Staying the Course ≠ Doing Nothing Forever

Yes, staying invested during market volatility is usually the right move, but does that mean your investments should go untouched for decades? Of course not. Your financial life isn't static, nor is the world around you. Life changes. Goals shift. The markets evolve. And your investment strategy needs to reflect that. Think of your portfolio as a garden. Staying the course means letting your plants grow, not digging them up every time a storm rolls in. BUT it doesn't mean ignoring weeds, forgetting water, or never pruning. Good gardeners check in regularly—so should good investors.

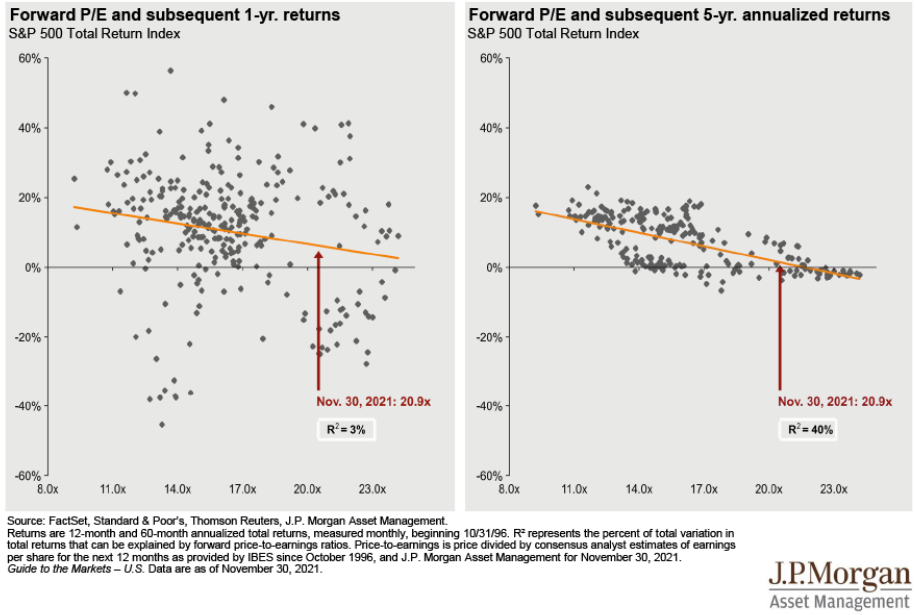

This chart below, created by my colleague, Nick Boguth, effectively illustrates the undeniable relationship between risk and return. While drawdowns can be unsettling, we are here to provide guidance and support during these uncertain periods. However, it is important to notice that significant periods of volatility are often followed by substantial growth. The blue line below signifies how markets have continued to grow despite volatility and drawdowns (orange line). While those drawdowns can be deep and painful to live through in the moment, you can see that they tend to be only temporary

What Staying the Course Really Means

It means sticking to a well-thought-out plan, not ignoring it altogether. It means:

Rebalancing regularly – Markets move, and over time, your portfolio drifts from its original allocation. Rebalancing brings it back in line with your risk tolerance and goals. Luckily, we are already doing this for you! We review accounts frequently throughout the year and rebalance when they deviate from your set goals.

Reviewing goals and timelines – Are you still saving for that early retirement? Has your timeline changed? Are you nearing a big purchase? Your investments should reflect those life updates. Guess what? We do this for you, too! These items are usually discussed during your Annual Review Meetings with your planner.

Avoiding emotional reactions – This one remains true. Don't let headlines or temporary downturns dictate your moves. We know this can be difficult, but again, staying calm isn't the same as being passive. We are always available to answer any questions that you may have.

The Bottom Line

Staying the course is about consistency, not complacency. The most successful investors stay engaged, review their plans periodically, and always keep the big picture in mind. So no, you don't need to micromanage your portfolio every week, but it shouldn't be stashed away or forgotten. Check in, stay informed, and above all else, trust the process.

Mallory Hunt is a Portfolio Administrator at Center for Financial Planning, Inc.® She holds her Series 7, 63 and 65 Securities Licenses along with her Life, Accident & Health and Variable Annuities licenses.

The information contained in this blog does not purport to be a complete description of the securities, markets, or developments referred to in this material. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Any opinions are those of Mallory Hunt and not necessarily those of Raymond James. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Investing involves risk and you may incur a profit or loss regardless of strategy selected. Every investor's situation is unique and you should consider your investment goals, risk tolerance and time horizon before making any investment. Prior to making an investment decision, please consult with your financial advisor about your individual situation.