Contributed by: Center Investment Department

Contributed by: Center Investment Department

Spring of 2022 feels as though it is bringing in a new wave of hope. There appears to be at least a reprieve (maybe nearing an end?) to the pandemic here in the U.S, and economic re-openings seem only to be limited by the number of staff members businesses can hire. However, the first quarter also brought many other headlines, including a severe escalation of the Russia/Ukraine conflict, increased oil prices and inflation, and higher interest rates.

It has been a rocky start to the year with a diversified portfolio ending -5.34% (40% Bloomberg US Agg Bond TR (Bonds), 40% S&P 500 TR (US Large company stocks), and 20% MSCI EAFE NR (Developed International)). There seemed to be nowhere to hide this quarter as volatility was present worldwide in equities and the fixed income markets.

Source: Morningstar Direct

Is This Market Decline Normal?

This chart shows intra-year stock market declines (red dot and number) and the market’s return for the full year (gray bar). A couple of takeaways from the below chart are important:

The market is capable of recovering from intra-year drops and finishing the year in positive territory.

This year’s correction thus far does not stick out as anything other than normally experienced corrections, even though the reasons for it may not feel normal.

Source: FactSet, Standard & Poor’s, J.P. Morgan Asset Management (Returns based on price index only and do not include dividends. Intra-year drops refer to the largesrtmarket drops from peak to trough during the year)

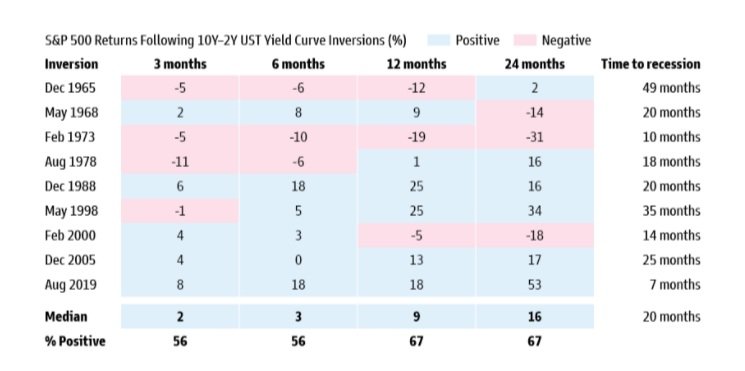

Yield Curve Inversion

You may have read that the yield curve briefly inverted toward the end of the quarter after the Federal Reserve raised interest rates for the first time in this newest interest rate cycle. If not, check out our blog.

Historically, an inverted yield curve has been a signal for a coming recession. Imperfect of a signal as it is, we do take notice. This is one of several parameters we utilize at The Center for making portfolio decisions. The good news is, there is usually time before a recession hits if it does. Now that this signal has been triggered, we have a series of other signals we watch for before determining any appropriate action. Next, we seek to follow through on the economy and technical analysis because, as the chart below shows, the S&P 500 can continue to deliver positive returns (over 3, 6, 12, and 24 months) after the yield curve inverts but before recession strikes.

Source: Goldman Sachs Global Investment Research

While we may not be able to control if a recession occurs or not, we certainly can help you prepare. Here is a checklist of potential action items to consider when they happen. Many of which we take care of for you already. Any questions? Don’t hesitate to reach out!

Is Inflation Sticky?

The answer is…it depends. It depends on which contributors to inflation you are looking at. Energy is a good example. The price of a barrel of oil had a large spike (up 30%) and pullback (down 25%) all during the month of March caused by the Russia/Ukraine conflict and sanctions put in place against Russia who is a large exporter of oil (especially to Europe). Before the Russia/Ukraine conflict, energy prices rose steadily with the economic re-opening and supply limitations put in place by OPEC. This volatile component can become a large detractor just as quickly as it became a large contributor. This is why the Federal Reserve prefers to filter this noise out for its decision-making purpose and focus more on Core CPI numbers instead that eliminate food and energy due to their volatile nature. As the year continues, we may see inflation coming from the green, red, and purple areas below start to abate, leaving us with roughly 4-5% inflation (still above the Federal Reserve’s target of 2%).

Source: BLS, J.P. Morgan Asset Management

Russia/Ukraine Conflict

We will speak for everyone in saying that we are saddened by the tragic events taking place overseas in Ukraine. We continue to hope for a quick, peaceful resolution.

Markets have been increasingly volatile as the conflict unfolds, but the U.S. stock market has been shockingly positive since Russia invaded Ukraine. The one-month period from February 24th to March 24th showed the S&P 500 up ~5%. Or maybe that is not shocking when you look at how markets typically react to global conflicts. If you attended our investment event in February, you would have already seen this data. Still, the average time it has taken the market to recover from geopolitical conflict-induced drawdowns is only 47 days.

The conflict between Russia and Ukraine is shaking up stock markets, commodity markets, and providing even more uncertainty to domestic inflation and monetary/fiscal policy. During these times, it is important to remember that financial plans are built to withstand uncertainties. Diversification is more important now than ever. We will continue to monitor these events and keep you informed as we make decisions that may or may not affect investment allocations.

Key Takeaways

To summarize, here is what happened in the first quarter:

Stocks and bonds struggled because of inflationary pressures.

Commodity-linked sectors and countries benefitted, but on the other hand, growth assets and commodity importers struggled.

Lastly, stating the obvious, the war in Ukraine has had a negative impact on Europe.

Now that we understand what happened, we are sure you want to know how we are responding.

We are monitoring our parameters to identify (if or) when it is necessary to adjust your bond to equity ratio and add duration back into the portfolio. Speaking of which, our parameters are telling us short bonds are still appropriate for investors. Remember, the higher the duration, the more a bond’s value will fall as interest rates rise. Consequently, we are maintaining a sleeve of your bond position in short-duration investments.

We are taking advantage of market volatility by tax-loss harvesting. Tax-loss harvesting helps minimize what you pay in capital gains taxes by offsetting your income.

Finally, we routinely review portfolios and rebalance them to capture cheap buying opportunities.

If you would like to gather more insight, we will include links to our most recent investment event and blogs. As always, we are here for you. Don’t hesitate to give us a call!

Explore More…

March FOMC Meeting: Rate Liftoff

Any opinions are those of the author and not necessarily those of Raymond James. The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. There is no assurance any of the trends mentioned will continue or forecasts will occur. The information has been obtained from sources considered to be reliable, but Raymond James does not guarantee that the foregoing material is accurate or complete. Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Investing involves risk and you may incur a profit or loss regardless of strategy selected. The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. stock market. The MSCI EAFE (Europe, Australasia, and Far East) is a free float-adjusted market capitalization index that is designed to measure developed market equity performance, excluding the United States & Canada. The EAFE consists of the country indices of 22 developed nations. The Bloomberg Barclays US Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs or other fees, which will affect actual investment performance. Individual investor's results will vary. Past performance does not guarantee future results. Diversification and asset allocation do not ensure a profit or protect against a loss. Dividends are not guaranteed and must be authorized by the company's board of directors. Special Purpose Acquisition Companies may not be suitable for all investors. Investors should be familiar with the unique characteristics, risks and return potential of SPACs, including the risk that the acquisition may not occur or that the customer's investment may decline in value even if the acquisition is completed. Investing involves risk and you may incur a profit or loss regardless of strategy selected. Past performance is not a guarantee or a predictor of future results. Raymond James and its advisors do not offer tax or legal advice. You should discuss any tax or legal matters with the appropriate professional.