Contributed by: Angela Palacios, CFP®, AIF®

Contributed by: Angela Palacios, CFP®, AIF®

Contributed by: Nicholas Boguth, CFA®, CFP®

Contributed by: Nicholas Boguth, CFA®, CFP®

Executive Summary

Markets faced early volatility driven by geopolitical tensions, higher oil prices, tariff uncertainty, and evolving Fed policy.

Stocks declined modestly (S&P 500 down ~4%), while bonds were essentially flat, cushioned by higher yields.

Oil and gold were volatile, reminding investors that even “safe haven” assets can move unexpectedly.

The Federal Reserve held rates steady, despite market swings in rate-cut and rate-hike expectations.

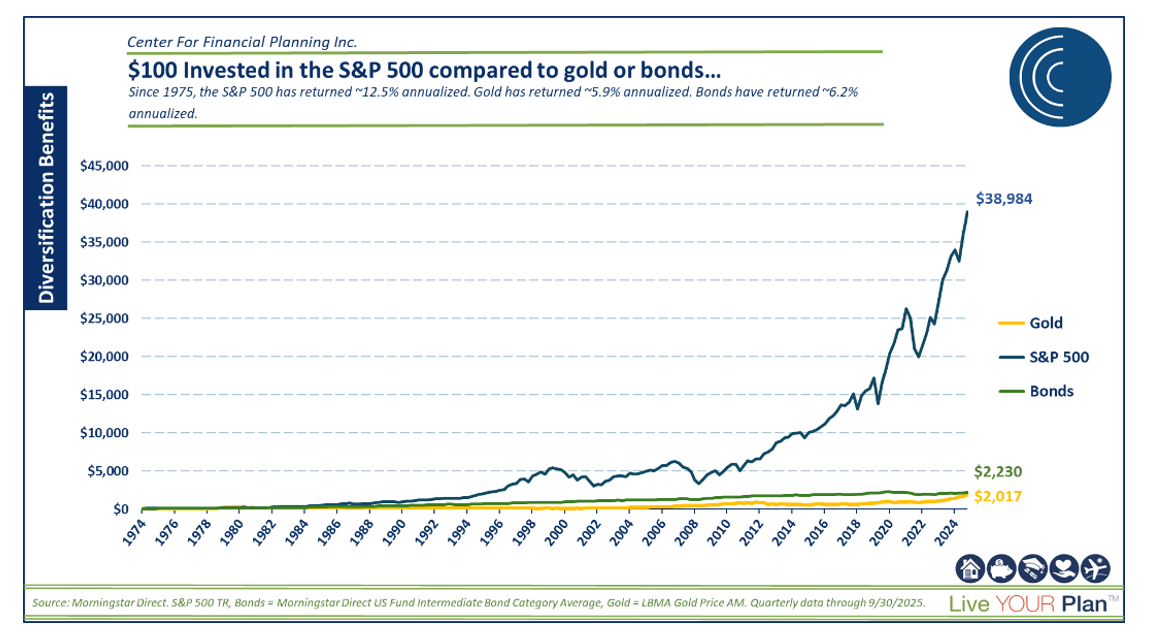

Diversification mattered—spreading risk across asset classes and sectors helped limit portfolio drawdowns.

Long-term investors are best served by staying disciplined, maintaining liquidity needs, and avoiding emotional decisions during short-term market noise.

Volatility is a normal part of investing. A thoughtful financial plan and a diversified portfolio remain the most reliable tools for navigating uncertain markets.

2026 is off to an eventful start, reminding us once again that volatility is a normal part of the investing journey. A wide variety of headlines, mostly geopolitical, have dominated the year so far, creating early volatility across equities, commodities, and even bonds. First, the U.S. military arrested the Venezuelan President Nicolás Maduro and his wife, forcing a change in leadership for the country. Gold and silver surged, while defensive sectors like U.S. energy and utility stocks rallied. Shortly after, the U.S. made statements about the possibility of controlling Greenland, which strained relations with Denmark and NATO partners. Lastly, the U.S. re-entered conflict in the Middle East as war broke out in the region with Iran. With traffic through the Strait of Hormuz restricted, global oil markets felt the impact as the price for a barrel of oil quickly spiked to well over $100 and hovered there for the remainder of the quarter.

Bonds, as measured by the Bloomberg US Aggregate Bond index, ended the quarter essentially flat at -0.05% while U.S. stocks (S&P 500) were down -4.33%. International markets and U.S. small-cap markets started the year with surprising strength, but they have given back much of those gains through March as the war escalated. Gold experienced the most volatility, rallying another 20% this year before giving nearly all of that back, and ended the quarter up only 5.7%. In our recent investment event, we discussed many of these headlines and noted that this is a midterm election year, which is usually marked by greater-than-average volatility but often ends positively.

Volatility Caused by Geopolitical Events

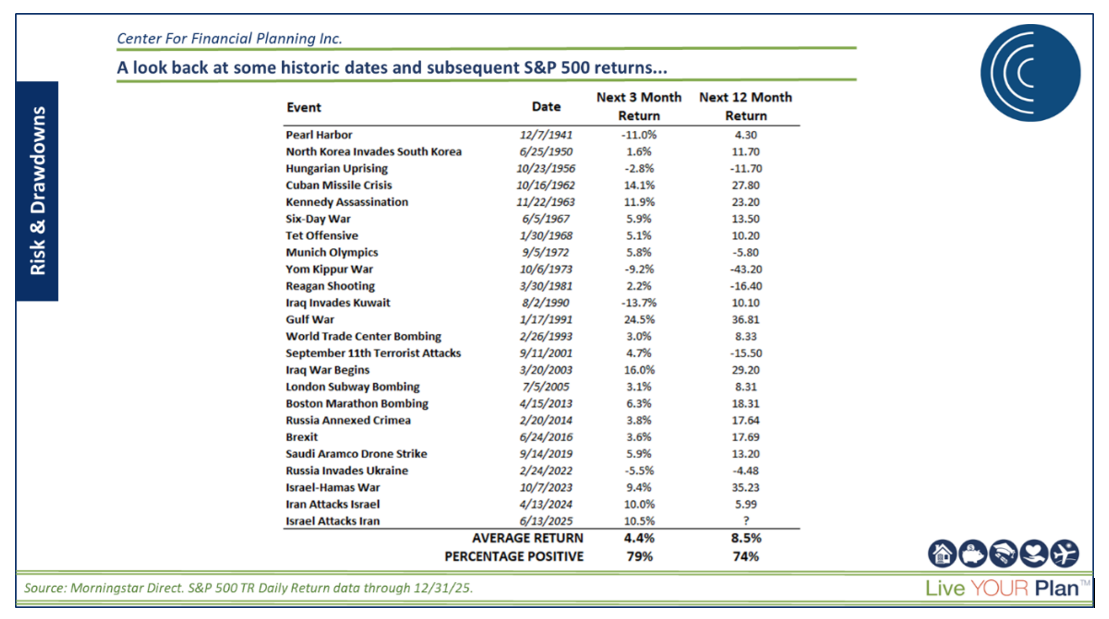

The above headlines can make investors want to act – maybe even sell their investments and stock up on cash under the mattress or gold bars in the safe. In times of stress, it is important to lean on history and data to guide the next best course of action. See below for stock returns 3 and 12 months after key conflicts over the past 100 years. Does the data surprise you?

Diversification and remaining invested are very important in times like these. While diversification doesn’t completely insulate you from drawdowns during the hard times, it does make them much more bearable and hopefully sets your portfolio up for a quicker recovery. Volatility is a normal part of investing. Remember, if we had no risk, there would also be no reward. It is the price we pay for long-term positive returns. Each year, volatility crops up for one reason or another, and temporary pullbacks are very normal.

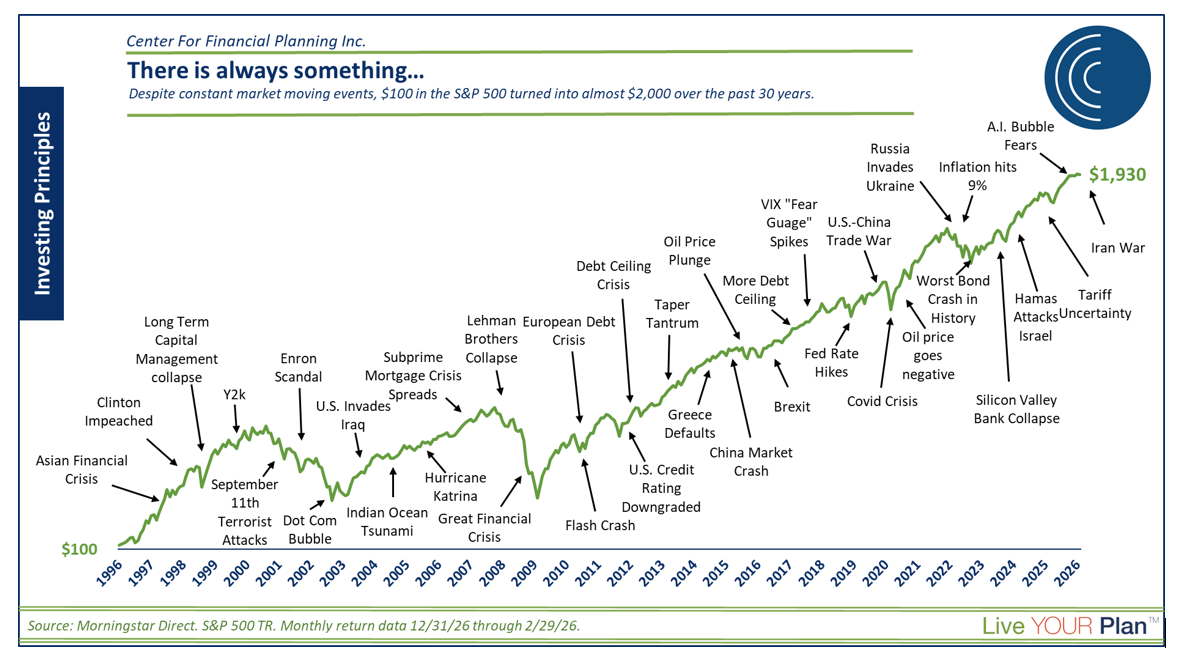

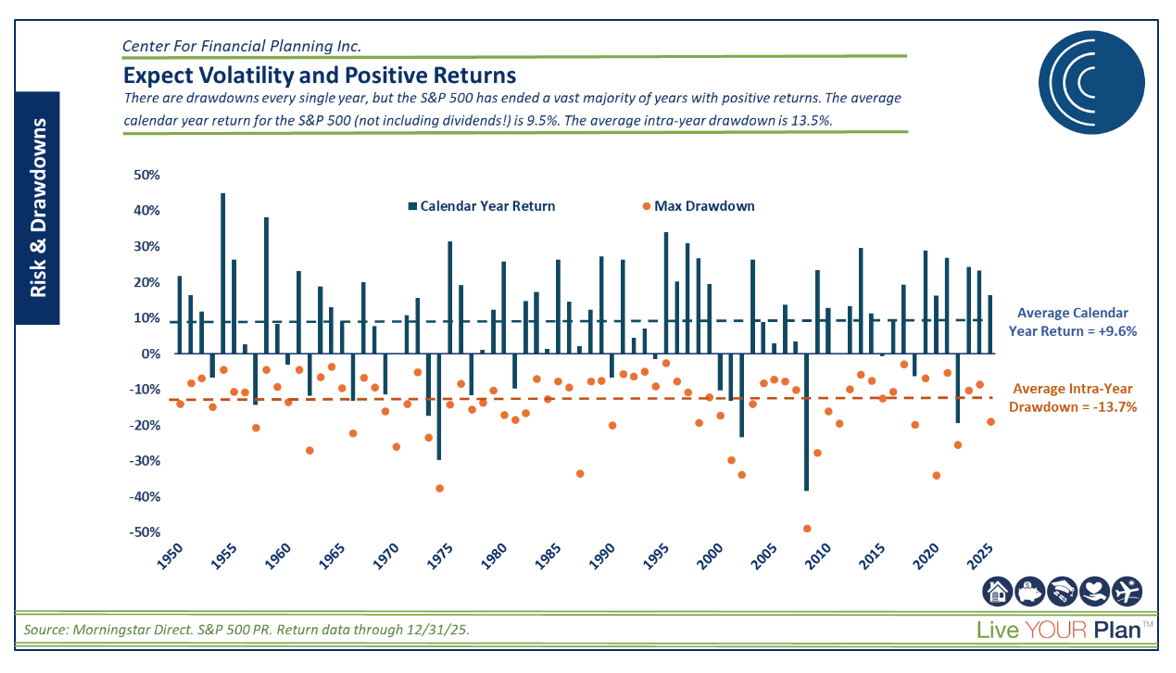

2025 and 2026 have been no exception. Liberation Day (political branding of tariff policies) caused a strong market pullback around the same time last year, followed by the Iran War this year. The chart below shows the regularity of pullbacks. The blue bars (overwhelmingly positive) are calendar year returns. The orange dots show how much the market fell WITHIN each calendar year. Some years only see 3% to 10% dips. Some years see dips of 10% to 50%. The “average” intra-year drawdown since 1950 is 13.5%. Despite those dips, the S&P 500 was positive ¾ of the time and averaged 9.5% per year.

For investors with long time horizons, these moments may serve as great entry points, especially if you have additional dollars to save. For those who depend on their assets, we have an action plan in place that was developed long before this volatility began. The thoughtful planning work we do with you helps ensure you have what you need for the next 6 months, a year, or even two years, already in cash or money market, which means you don’t have to sell into market volatility.

Federal Reserve and Interest Rates

The Federal Reserve (The Fed) has faced political pressure to cut interest rates while it navigates stubborn inflation, a weakening labor market, and the economic consequences of the war in Iran. The Fed opted to hold interest rates steady at 3.5%–3.75% through its January and March meetings, even as oil‑price spikes linked to Middle East conflict complicated its inflation outlook. It is important to remember that the Fed focuses on core PCE, which strips out inflation pressures from energy and food because they are typically so volatile. Inflation fears and concerns that the Fed could raise short-term interest rates have picked up again amid the spike in oil prices. I think we all immediately remember the 1970s era of inflation when we hear that oil is getting expensive and start to worry. As of now, this spike has been short-lived, and if the Straits of Hormuz reopen soon and oil starts moving again, we should see oil prices start to come back down. Short-term spikes usually don’t flow through to core PCE inflation in a meaningful way. However, if oil remains scarce and prices remain high, you will start to see the higher energy costs leak through to other areas of the economy, which would then be reflected in higher core PCE.

The bond market immediately jumped to the conclusion in March that the latter would happen, and the Fed would be staring at rising inflation numbers, and then further assume the Fed would start raising interest rates again to combat this inflation. We think it is far too early to assume this will happen. We entered the year with bond and equity markets pricing in 1 or 2 rate cuts by the end of this year, and now the market is pricing in a rate increase before year's end. This change in expectations is why bonds have had a negative month of returns. However, it is important to note that this isn’t the start of a 2022 bond market again. Now we are starting from a place of much higher yields, and we still have a robust interest rate being paid to us every month to compensate for some volatility.

Despite market assumptions, Fed officials continue to project one rate cut later in 2026, but internal disagreement continues, and if Kevin Warsh is confirmed by the Senate to take over in May, opinions could shift. It is important to remember that no single person sets this policy. There are 12 voting members of the Federal Open Market Committee (FOMC) who determine the fate of interest rates. The Chairman is simply the public representative of this board, and the chairperson only has 1 vote like everyone else and has no veto power.

At the same time, political pressure from President Trump on the Fed continues, as he publicly called for an immediate rate cut amid market volatility driven by war. Chair Jerome Powell, nearing the end of his term, emphasized that the Fed is still assessing the impact of the Iran war, elevated oil prices, and mixed economic data, and warned that the path ahead remains deeply uncertain. With leadership transitions approaching and geopolitical risks rising, the Fed’s next move remains far from clear—fueling market anxiety and adding to the perception that 2026 has become one of the most unpredictable years for Fed policy in over a decade.

Long Term Versus Short Term Interest Rates and Mortgage Rates

While the Fed does set interest rate policy, it is important to remember that it only sets short-term rates. Intermediate and long-term interest rates are driven more by supply and demand. Many have hoped that lower short-term rates would equate to lower mortgage rates. While rates have come down over the past 9 months, they have recently (in March) drifted back upward, causing new home buyers to pause. Earlier this quarter, 30-year mortgages had fallen below 6%, but they have drifted back to the mid-6 % range, nearly halting mortgage applications.

Private Credit Fears

Over the past few years, we have gotten many questions on private credit. We are constantly kicking the tires on different investment opportunities and trying to understand if they deserve a spot in your portfolio. The allure of 10%+ interest rates and little volatility sounded very tempting, but it was the first red flag in our review. Limited liquidity also had alarm bells swirling in our heads. Usually, if something sounds too good to be true, it often is. Private credit is no exception. Many dove in, thinking there would be little volatility and a great income stream. The problem with a limited liquidity product is just that, you usually can’t access your money when you most want it. As there were notable headlines about private credit borrowers, these private credit funds faced many redemption requests that they could not fulfill. Imagine wanting to sell an investment and being told no. That fear then starts to snowball, and more investors request redemptions, snowballing the issue and the headlines. We recognized this product for what it is: for high-net-worth investors with very long time horizons who can wait out redemption limitations without needing the cash. Even then, they aren’t guaranteed to pay you a premium investment return. The headlines are likely to continue escalating around these products as barriers to selling persist and securities in the portfolios are marked down to their actual values.

Artificial Intelligence

A.I. news continues to drive headlines and move markets. Companies that are driving the technology forward continue to share new developments and innovations that can be both exciting AND nerve-wracking. There is no shortage of opinion pieces predicting what the future holds for the technology, ranging from “minor” to “world-changing”. This uncertainty has shown up in financial markets, as there is some dispersion in stock prices lately. Not everything is moving in unison…which is healthy! We would not want to see dot-com bubble-era behavior, where any stock that mentioned A.I. was immediately rewarded. Certain companies’ stock prices have fallen following announcements of large A.I. spending plans, while others have reacted positively. Demand for “chips” is driving strong earnings expectations in the semiconductor industry, but there is concern about circular spending, where companies are just paying each other back and forth, and that may not be sustainable. There has also been some major volatility among individual stock names as competitive moats come under attack from A.I. Utilities and commodities are affected as “datacenter” plans with mind-blowing power needs continue to develop.

This is a major theme that affects many parts of the market. With any innovation, uncertainty follows, and all investors can do is invest accordingly. As far as our portfolios go, we continue to monitor valuations and expectations for the stocks and bonds that are directly affected. This quarter's volatility has actually made valuations more attractive. We get the question, “Is this a bubble?” a lot…and we just don’t see it across the whole market. Sure, there might be individual companies trading at extreme valuations, but it certainly isn’t across the entire market. It might surprise you to hear that, for example, Microsoft ended the quarter in a 31% drawdown from its prior high! It is one of the largest holdings in the S&P 500, but due to performance in other sectors, the index was still only down ~4% in Q1. To us, that is yet another example of diversification (in this case, sector diversification within the S&P 500) leading to better outcomes for investors.

Tariff Update

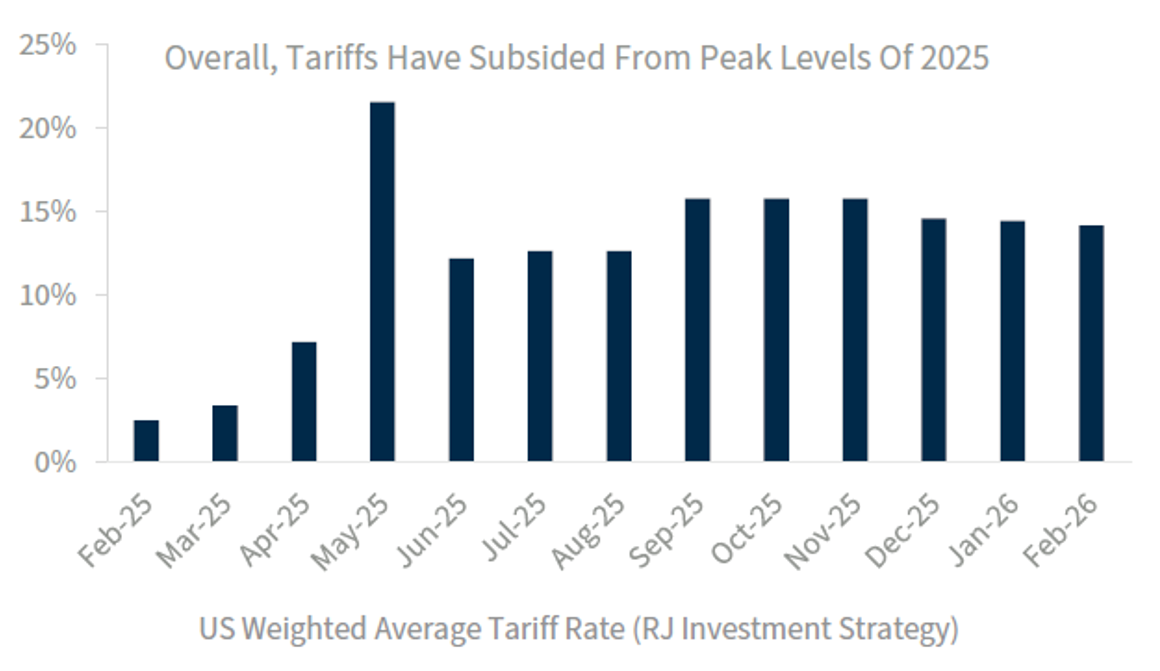

Trump’s tariffs were another source of volatility in the first quarter. The Supreme Court ruled that a portion of Trump's tariffs, the ones imposed on specific countries, were unlawful. Trump’s initial justification for imposing those tariffs as a national “emergency” did not hold up in the Supreme Court, so those tariffs were removed. He immediately responded to this ruling by imposing new temporary tariffs of 10%, then later 15%. Ultimately, this is a fluid situation that is adding to the uncertainty in the stock and bond markets. Companies have to navigate pricing and supply chain issues arising from tariff uncertainty, and there is still the lingering question of whether tariff refunds will be paid out.

Overall, it seems we can expect tariffs to remain in place for now, which will ultimately provide another revenue stream for the U.S. government but lead to higher prices for U.S. consumers. Time will tell how these tariffs will change going forward, whether they will remain in place long-term or be used more as a bargaining chip to make deals with other countries.

Gold Crash?

Another surprising market move in Q1 came from Gold. Gold started the year continuing its growth, hitting a new all-time high of almost $5,600 near the end of January! Then it fell 20% from its high over the next month and a half, bottoming out near $4,200 on March 23rd. It rallied slightly and ended the quarter near $4,600/oz.

The market can surprise us more often than we think. Gold is often considered a “safe haven” asset, which you would expect would RALLY in the event of something like, I don’t know, the unknowns of a war in the Middle East. But that is not how gold reacted this past quarter; in fact, headlines at the very end of the quarter hinted at an off-ramp from the conflict with Iran, and gold actually rallied on the news, similarly to stocks! Not exactly the movement you would expect from a “safe haven” asset.

Gold is an uncorrelated asset for better or worse. It has been on an amazing run over the past few years and just began experiencing some volatility this past quarter. Like any asset, consider the risks before investing, and understand your unique situation and financial plan to determine if, where, and how gold might fit into your portfolio.

Thank you for taking the time to read this quarter’s investment commentary. There is a lot of noise in the markets, and we believe that a thoughtful financial plan, paired with a disciplined investment process, is more important than ever. Please don’t hesitate to reach out to your financial advisor or anyone on our team here at The Center with any questions. We’re here to help and would be delighted to have a conversation.

Angela Palacios, CFP®, AIF®, is a partner and Director of Investments at Center for Financial Planning, Inc.® She chairs The Center Investment Committee and pens a quarterly Investment Commentary.

Nicholas Boguth, CFA®, CFP® is a Senior Portfolio Manager and Associate Financial Planner at Center for Financial Planning, Inc.® He performs investment research and assists with the management of client portfolios.

Any opinions are those of Angela Palacios, CFP®, AIF® and Nick Boguth, CFA®, CFP® and not necessarily those of Raymond James. The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. There is no assurance any of the trends mentioned will continue or forecasts will occur. The information has been obtained from sources considered to be reliable, but Raymond James does not guarantee that the foregoing material is accurate or complete. Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Investing involves risk and you may incur a profit or loss regardless of strategy selected.

The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. stock market. The Russell 2000 Index measures the performance of the 2,000 smallest companies in the Russell 3000 Index, which represent approximately 8% of the total market capitalization of the Russell 3000 Index. The MSCI EAFE (Europe, Australasia, and Far East) is a free float-adjusted market capitalization index that is designed to measure developed market equity performance, excluding the United States & Canada. The EAFE consists of the country indices of 22 developed nations. The Bloomberg Barclays US Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs or other fees, which will affect actual investment performance. Individual investors’ results will vary. Investing in oil involves special risks, including the potential adverse effects of state and federal regulation and may not be suitable for all investors. Past performance does not guarantee future results. Diversification and asset allocation do not ensure a profit or protect against a loss. Investing involves risk and you may incur a profit or loss regardless of strategy selected. Past performance is not a guarantee or a predictor of future results. Raymond James and its advisors do not offer tax or legal advice. You should discuss any tax or legal matters with the appropriate professional.

Gold is subject to the special risks associated with investing in precious metals, including but not limited to: price may be subject to wide fluctuation; the market is relatively limited; the sources are concentrated in countries that have the potential for instability; and the market is unregulated.