It is summer time! So, if you get a few minutes in between all of the outdoor activities here are 7 quick financial planning strategies to review. As always, if we can help tailor any of these to your personal circumstances feel free to reach out.

By now you have heard there is a new tax law. Because we will not experience the actual affects until next April, many of us are not sure how it applies to our specific circumstances.

Do a quick tax projection with your tax preparer and check your tax withholding. Many of us will have an overall tax decrease – but withholdings from our paychecks also went down. Do not get caught off-guard. More importantly, some folks will see higher taxes due to the new limitations on certain itemized deductions. Combine this with lower withholding and you have a double whammy (read: you will be writing a bigger check to the IRS).

Lump and clump itemized deductions. The standard deduction has increased to $24k for married couples filing jointly. In addition, miscellaneous itemized deductions have been removed completely. $10k cap. For some. Lumping charitable deductions in one year to take advantage of itemizing deductions and then taking the standard deduction for several years might be best.

Utilize QCD’s. If you are over age 70.5 and making charitable contributions, you should consider utilizing QCD. Don’t know what QCD stands for? Call us now.

Consider partial ROTH conversions to even out your tax liability. If you are retired, but not yet age 70.5 (when RMD’s start). Don’t know what an RMD is? Talk with us today! If you are in this group, multiyear tax planning may be beneficial.

Most estates are no longer subject to the estate tax given the current exemption equivalent of $11.2M (times 2 for married couples). However, income taxes remain an issue to plan around. One of my favorites: Transfer low basis securities to aging parents and then receive it back with a step up in basis. If you think you might be able to take advantage of this let us know.

Review your distribution scheme in your Will or Trust. Are you using the old A-B or marital/credit shelter trust format? Do you understand how the increased exemption affects this strategy?

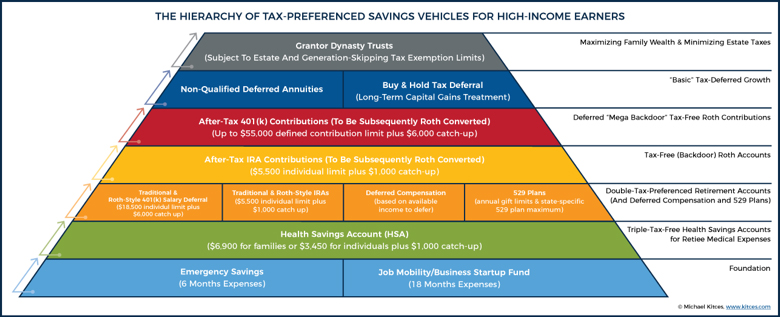

How should high-income folks prioritize their savings?

Are you in the new 37% marginal bracket? If so, consider contributing to a Health Savings Account IF eligible. Next, consider making Pretax or traditional IRA/401k contributions. However, if you reasonably believe that you will be in the highest marginal tax bracket now AND in retirement – then the ROTH may be suggested. Know that for the great majority of us this will not be the case. Meaning, we will be in a lower bracket during our retirement years than our current bracket. Next, use Backdoor ROTH IRA contributions. If your employer offers an after tax option to your 401k plan, take advantage of it. You can then roll these funds directly into a ROTH. Next, consider a non-qualified annuity that provides tax deferral of earnings growth followed by taxable brokerage account.