The holidays provide us with rare opportunities to gather with family. This is a time to check in with older adult parents to see how things are going and to see what might be changing. Often, we will notice that time (and/or age) are beginning to make everyday life a little more challenging for our parents. This is the perfect time to ask your parents about their plans for their future.

The holidays provide us with rare opportunities to gather with family. This is a time to check in with older adult parents to see how things are going and to see what might be changing. Often, we will notice that time (and/or age) are beginning to make everyday life a little more challenging for our parents. This is the perfect time to ask your parents about their plans for their future.

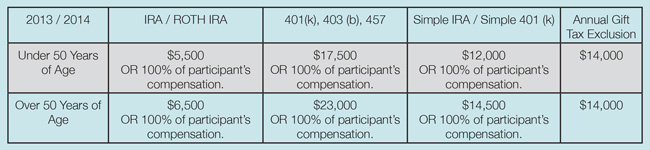

Things to discuss with your parents may include:

- Where do they plan to live as they age?

- How do they envision living their future lives (activities, future care, etc.)?

-

Do they have their financial lives organized and documented to make future planning easier? If not, here is a great resource to give them: https://static1.squarespace.com/static/54341a03e4b08690c01bc8de/54dcf260e4b018fb5adfbec4/54dcf261e4b018fb5adfc6e8/1303923614337/record_system.pdf

- Are their legal documents up-to-date so that their current wishes will be carried out?

If having these conversations makes you feel uneasy, you are not alone. However, giving your parents the opportunity to express their desires and helping them to put an actual plan in place to make their plans a reality is an invaluable gift. And what better time than the holidays to give that gift?

Contact your financial planner for tips on holding these conversations or to schedule a family planning meeting.

Sandra Adams, CFP® is a Financial Planner at Center for Financial Planning, Inc. Sandy specializes in Elder Care Financial Planning and is a frequent speaker on related topics. In 2012 and 2013, Sandy was named to the Five Star Wealth Managers list in Detroit Hour magazine. In addition to her frequent contributions to Money Centered, she is regularly quoted in national media publications such as The Wall Street Journal, Research Magazine and Journal of Financial Planning.

Five Star Award is based on advisor being credentialed as an investment advisory representative (IAR), a FINRA registered representative, a CPA or a licensed attorney, including education and professional designations, actively employed in the industry for five years, favorable regulatory and complaint history review, fulfillment of firm review based on internal firm standards, accepting new clients, one- and five-year client retention rates, non-institutional discretionary and/or non-discretionary client assets administered, number of client households served.