Contributed by: Angela Palacios, CFP®

Roll yield is a term that you may have heard lately in the financial news. No, I am not talking about Cubans and cigars. I am referring to a potentially profitable bond trading strategy that can be employed to enhance returns of a bond portfolio during a rising interest rate environment.

The Traditional Buy and Hold Bond Strategy

With interest rate increases supposedly just around the corner, investors fear negative or very low returns out of their bond positions. Furthermore, there are many proponents of buying individual bonds only during a rising interest rate environment. This strategy offers certainty of getting your principal back upon maturity if the creditor doesn’t default. However, when the bond yield curve is sloping upward there is another strategy that could be employed successfully and potentially create better long term returns than the buy and hold strategy.

How the Roll Yield Bond Strategy is Different

Roll yield is often thought of hand-in-hand with the futures market. In the futures market when you are buying a contract on the price of coffee for example, you are always paying either more or less then coffee is actually trading at in that moment (this is referred to as the spot price). If you are paying less for the contract than the current spot price, you can then achieve a positive roll yield or price increase as that contract gets closer and closer to maturing at the spot price (assuming the spot price doesn’t change) as shown by the green line in the chart below.

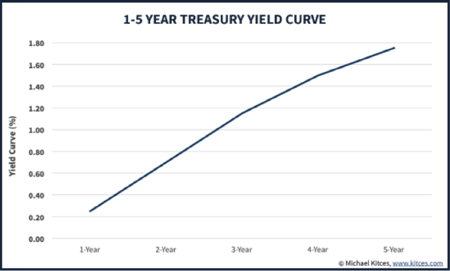

In the bond market this concept is similar but works a bit differently. When you buy a bond, for example a 5 year treasury bond, you pay $1,000 for this bond and in return get a set rate of interest, I will use1.75% for example. If the yield curve is upward sloping that means that bonds maturing in less than 5 years should pay some interest rate less than 1.75% as you aren’t tying your money up for as long. For example, a 4-year bond could yield 1.5%. See the chart below for an example of an upward sloping yield curve.

As you hold your 5-year treasury it grows closer to maturity every day and eventually your 5 year bond turns into a 4 year bond, 3 year bond and so on until it matures. If rates don’t change over the first year, you now possess a 4 year bond that yields 1.75% when all other 4-year treasury bonds that are issued are only paying 1.5%. The interest rate premium means people want your bond more and are willing to pay more money for it. This results in price appreciation or a capital gain on the bond. At that time, you could sell the bond and collect the price appreciation in addition to the 1.75% in interest that you collected over the past year.

The chart below shows a hypothetical example of owning 100 of these bonds. The blue area is the 1.75% interest that you receive each year. You can see that it stays level each year until maturity. However, in the first year you see that there is a red area, or addition to your return, from capital gains of the price going up due to the nature of the process explained above. You could sell your 100 bonds that in 4 years will mature again at $100,000 or sell it for $101,000 and over the first year collect a total of $1,750 in interest plus $1,000 in capital gains making your return on the $100,000 investment.

Then you could re-invest in a new 5 year bond still paying 1.75% interest again. The reason you may want to make this transaction is when you get closer to the bond maturing you will have to lose that increase in price because you will only receive your $1,000 back from the US Treasury that you paid originally for the bond and therefore, the bond price will come back down as investors know this will happen and will be unwilling to pay more for the bond. This is shown in the chart above as the annual loss (red area) in years 4 and 5 on the bond.

Large Bond Managers vs. the Individual Investor

A buy-and-hold investor would give up this potential increase in returns in the early years of holding the bond by not selling and locking in the price appreciation. However, this strategy can be difficult to pay off for an individual investor because you are dealing in smaller lots of individual bonds and thus you pay commissions and are subject to bid/ask spreads that could make it too costly to trade and take advantage of roll yield. Large bond managers can often successfully pull this off because they have pricing power due to the sizes of the bond lots they trade.

If rates rise too quickly or only certain parts of the yield curve increase, this type of strategy may not pay off over a buy-and-hold investor. An investor needs to weigh whether or not they would prefer the certainty of the individual bond or if they would prefer to outsource to a manager to implement potential strategies such as roll yield to enhance returns over time.

Angela Palacios, CFP® is the Portfolio Manager at Center for Financial Planning, Inc. Angela specializes in Investment and Macro economic research. She is a frequent contributor to Money Centered as well as investment updates at The Center.

Sources: http://www.futurestradingpedia.com/futures_roll_yield.htm https://www.kitces.com/blog/how-bond-funds-rolling-down-the-yield-curve-help-defend-against-rising-interest-rates/

This material is being provided for information purposes only and is not a complete description, nor is it a recommendation.The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. Any opinions are those of Angela Palacios and not necessarily those of Raymond James. Investing always involves risk, including the loss of principal, and futures trading could present additional risk based on underlying commodities investments. There are special risks associated with investing with bonds such as interest rate risk, market risk, call risk, prepayment risk, credit risk, reinvestment risk, and unique tax consequences. To learn more about these risks and the suitability of these bonds for you, please contact our office.