Contributed by: Angela Palacios, CFP®, AIF®

Contributed by: Angela Palacios, CFP®, AIF®

While trying to time the market may seem tempting during times of volatility, investors who attempt to, run the risk of missing periods of quality returns, likely leading to significant adverse effects on the ending value of a portfolio.

The image below illustrates the value of a $100,000 investment in the stock market during the 2007–18 period, which included the global financial crisis and the recovery that followed. The value of the investment dropped to $54,381 by February 2009 (the trough date), following a severe market decline. If an investor remained invested in the stock market over the next nine years, however, the ending value of the investment would have been $227,993. If the same investor exited the market at the bottom, invested in cash for a year, and then reinvested in the market, the ending value of the investment would have been $148,554. An all-cash investment at the bottom of the market would have yielded only $56,122. The continuous stock market investment recovered its initial value over the next three years and provided a higher ending value than the other two strategies. While all recoveries may not yield the same results, investors are well advised to stick with a long-term approach to investing.

Sometimes it can feel very difficult to stay invested!

Crises and Long-Term Performance

Economies and markets tend to move in cycles, and any stock market can have a downturn once in a while. Most investors lose money when the stock market goes down, but some people may think they can time the market and gain. For example, an investor may aim to buy in when the market is at the very bottom and cash out when the recovery is complete, thus enjoying the entire upside.

The problem with this type of reasoning is that it’s impossible to know when the market hits bottom. Most investors panic when the market starts to decline, then they decide to wait and end up selling after they have already lost considerable value. Or, on the recovery side, they buy in after the initial surge in value has passed and miss most of the upward momentum.

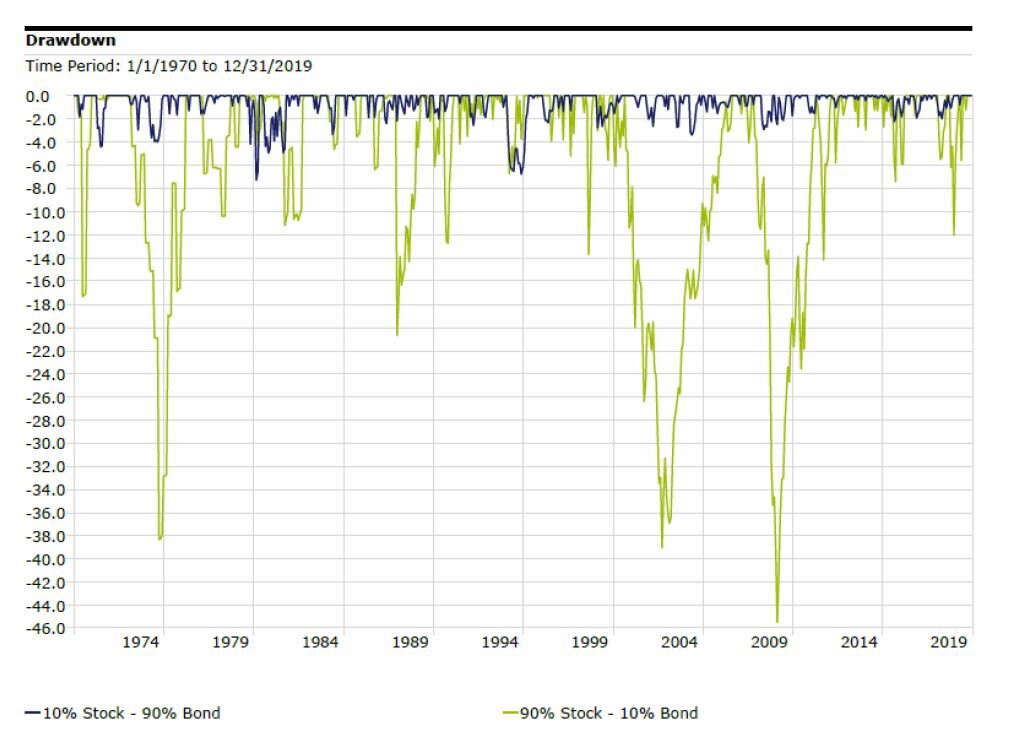

The graph illustrates the growth of $1 invested in U.S. large stocks at the beginning of 1970 and the four major market declines that subsequently occurred, including the recent banking and credit crisis. Panic is understandable in times of market turmoil, but investors who flee in such moments may come to regret it.

Each crisis, when it happens, feels like the worst one ever (the most recent one in 2008, as evidenced by the image, actually was). When viewed in isolation on the lower-tier graphs, each decline appears disastrous. However, historical data suggests that holding on through difficult times can pay off in the long run. For example, $1 invested in January 1970 grew to $117.05 by December 2018, generating a 10.2% compound annual return. And in the past, when looking at the big picture, every crisis has been eclipsed by long-term growth.

Please don’t hesitate to reach out to us when you are feeling uneasy during market volatility. We are here, working for you!

Angela Palacios, CFP®, AIF®, is a partner and Director of Investments at Center for Financial Planning, Inc.® She chairs The Center Investment Committee and pens a quarterly Investment Commentary.

Returns and principal invested in stocks are not guaranteed. Stocks have been more volatile than bonds or cash. Holding a portfolio of securities for the long term does not ensure a profitable outcome and investing in securities always involves risk of loss. About the data: Stocks are represented by the Ibbotson® Large Company Stock Index. An investment cannot be made directly in an index. Four market crises defined as a drop of 25% or more in the index. Return is represented by the compound annual return. Recession data is from the National Bureau of Economic Research. The market is represented by the Ibbotson® Large Company Stock Index. Cash is represented by the 30-day U.S. Treasury bill. An investment cannot be made directly in an index. The data assumes reinvestment of income and does not account for taxes or transaction costs. Performance of a hypothetical investment does not reflect transaction costs, taxes, or returns that any investor actually attained and may not reflect the true costs, including management fees, of an actual portfolio. Changes in any assumption may have a material impact on the hypothetical returns presented. Illustration does not include fees and expenses which would reduce returns. The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Any opinions are those of Angela Palacios, and not necessarily those of Raymond James. Expressions of opinion are as of this date and are subject to change without notice. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Investing involves risk and you may incur a profit or loss regardless of strategy selected. Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs or other fees, which will affect actual investment performance. Individual investor's results will vary. Past performance does not guarantee future results. Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation.