Diversified portfolios continue their uphill battle as the U.S. Stock market continues to be one of the few sources of positive returns this year. In August, the current bull market became the longest on record since World War II by avoiding a 20% drawdown during that time. Recently, the equity markets fell sharply even though the near-term prospects for the economy remain strong, but there are concerns about the November election, trade policy disruptions, FED policy and labor market constraints. Increased volatility and see-sawing markets are likely to continue in the near term.

*annualized

Bonds have continued to be under the pressure of gradually rising interest rates. Since December 2016, the Fed has raised short-term rates by .25% during 8 of the last 15 meetings. The last time we experienced rising interest rates was 2004-2006. During this period, the Fed raised short-term rates by .25% in 17 consecutive meetings in contrast! This time, they are taking a far more measured pace trying to increase borrowing costs for businesses and consumers to keep the economy from overheating.

International and especially emerging markets are struggling the most this year due to trade war concerns and a strong U.S. dollar even though they were the darlings of 2017.

Trade War Tracking

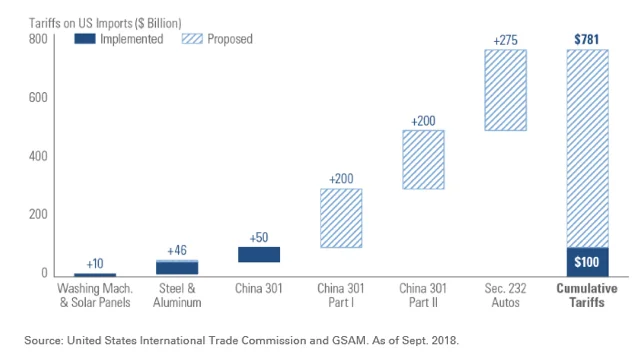

Since the trade war is at the top of the headlines each day, I thought it would be interesting to share a scorecard. The below chart shows the tariffs that are still only in the proposal state (diagonal lines) and tariffs that have been put into place. You can see that only a small amount had been implemented before September. On September 21st, the next $200 Billion of tariffs were put into place (China 301 Part 1). These are tariffs on an extensive list of goods and will start at a 10% tariff, escalating to a 25% tariff in January 2019. China retaliated by placing tariffs on another $60 Billion in U.S. goods. This list was smaller and the amount of tariffs placed on them was lower than the market anticipated which is why we didn’t see any negative reactions from the stock market during this round.

While we are also actively negotiating trade policies with many countries, the focus and largest amount of potential tariffs are against Chinese imports. According to the office of the U.S. Trade Representative “The United States will impose tariffs on…Chinese imports and take other actions in response to China’s policies that coerce American companies into transferring their technology and intellectual property to domestic Chinese Enterprises. These policies bolster China’s stated intention of seizing economic leadership in advance technology as set forth in its industrial plans, such as ‘Made in China 2025.’”

While markets are more volatile this year seeming to be swayed by the latest tariff headline daily, local markets are still boasting 10.56% returns on the S&P500 for the year through the end of September. This says to us that markets think this trade war is survivable and possibly even beneficial to the U.S. While tariffs are generally a negative for an economy over the long-term, investors often, only see the short-term benefits these types of strong-arm policies can bring.

The point of free trade is that each group of producers focus on what they are best at and can produce the most efficiently (also at the lowest price/best quality).They can then sell their products and use the money to purchase what they need from the most efficient producer.This process usually stretches your dollar the farthest when it comes to purchasing power.Tariffs place an additional tax on the consumer as they usually result in higher prices for us or reduced margins for companies (or a combination of the two).We don’t share the markets rosy outlook, as we believe this trade war will result, eventually, in inflation and supply chain disruptions.It takes time to ramp up production domestically of products that become too expensive to import.When companies face the uncertainty of what retaliatory actions are coming next, they are apprehensive to make the investments required to ramp up local production in the first place.

Unemployment

We also have to consider that the unemployment rate is back to very low levels (blue line shows below 4% unemployment) and participations rates (gray bar) remain steady. Where are we going to get all of the new workers required to start producing items locally rather than importing?

We don’t think this is how Trump foresees the end game. He hopes to force China to remove the tariffs they have historically imposed on our goods to put us on a level playing field of no tariffs, no subsidies and preventing intellectual property drain. Whether he is right and China will be forced to come to the negotiation table remains to be seen. Volatility should continue at slightly higher levels if this trade war continues to ramp up.

Politics

Mid-term elections are coming up, and that always puts politics at the top of everyone’s minds. There is also fear of impeachment that we often hear from clients and how that could affect portfolios. Impeachment is the process where the House of Representatives through a simple majority brings charges against a government official. After the government official is impeached, the process then moves to the Senate to try the accused. This must pass the Senate by a 2/3’s majority vote. If this happened, President Trump would be removed from the office, and the Vice President would take his place.

There is little to refer to in recent history to understand how markets would react here in the U.S. if this were to happen. Bill Clinton was impeached in 1998, and Richard Nixon resigned during the Impeachment proceedings but was never actually impeached. There have been recent unsuccessful attempts to impeach Donald Trump, George W. Bush, and, yes, even Barack Obama. When Bill Clinton was impeached markets were down in bear market territory (over 20% peak to trough on the S&P 500) for a short time before it rallied back. The Russian Ruble Crisis also occurred at the same time, so it is hard to say that the impact to markets was solely due to the impeachment process. So while President Trump likes to boast that the “Markets will crash and that everyone will be poor” if he were impeached that is likely not the case.

While we don’t think this has a high likelihood of happening, if it did, short-term volatility would probably occur while there is uncertainty and this is one of the many reasons why we maintain a diversified portfolio. If stocks retreated, it is likely that our bond portfolios would perform well and even a possibility that international investments would strengthen in the face of a weaker dollar. We believe a diversified portfolio with short-term needs set aside in cash or cash equivalents is one of the most effective solutions to an extremely rare event like this.

While this bull market may be getting old, it is important to remember they do not simply die of old age; rather they are killed by recessions.The yield curve is getting dangerously close to inverting but has not, thus not signaling a recession…yet.We are keeping a close eye on the yield curve and trade war as these items could quickly spill us over into a risk of recession. Markets can breeze along seemingly unconcerned by these types of risk until they aren’t.When sentiment swings from optimistic to pessimistic, it can happen almost overnight.As a result, we continue to maintain that having a diversified portfolio is extremely important.We are actively taking advantage of rebalancing opportunities to make sure your portfolios are prepared.If you have any questions or would like to speak with us more on these topics, please don’t hesitate to reach out to us!

Thank you for your continued trust!

On behalf of everyone here at The Center,

Angela Palacios, CFP®, AIF®

Director of Investments

Financial Advisor, RJFS

Angela Palacios, CFP®, AIF® is the Director of Investments at Center for Financial Planning, Inc.® Angela specializes in Investment and Macro economic research. She is a frequent contributor The Center blog.

The foregoing information has been obtained from sources considered to be reliable, but we do not guarantee that it is accurate or complete, it is not a statement of all available data necessary for making an investment decision, and it does not constitute a recommendation. Any opinions are those of Angela Palacios and not necessarily those of Raymond James. Investing involves risk and you may incur a profit or loss regardless of strategy selected, including diversification and asset allocation. The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. stock market. Indices are not available for direct investment. Any investor who attempts to mimic the performance of an index would incur fees and expenses which would reduce returns.