As we enjoy fall, and the kids are excited for Halloween, the end of the year is right around the corner! Here is a summary of what occurred in markets over the past quarter, and what we think may come before year-end.

Executive Summary

It has been a strong quarter for U.S. equities, and the odds seem to be in our favor for this to continue, but a slowing economy and the trade war could, at any moment, derail growth.

Bond markets have offered a haven to the increased market volatility, and they have experienced above-average returns as the Federal Reserve (the Fed) has begun lowering rates this year. As markets have marched on, we have rebalanced and increased duration within bonds to more strongly offset market volatility (this area tends to zig when the markets zag).

Investors have been overly punitive to international markets.

Economic indicators continue to soften.

With impeachment possible, headlines will contribute to volatility, but conviction/removal of President Trump remains unlikely as this requires a two-thirds vote in the Senate.

At these historically low-interest rates, federal debt is now far more affordable to service than it was 20 years ago.

Remember that our portal offers a current view of your asset allocation and returns, and offers a vault to securely transfer documents to us! Also, search for us in the App Store under “Center for Financial Planning” for smartphone access to the portal.

U.S. Equity Markets

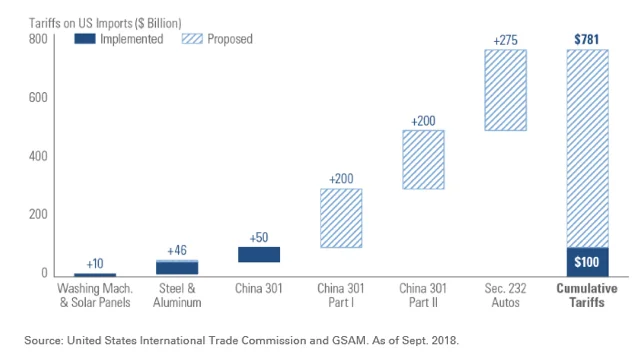

Historically, the third quarter of the year is the most difficult for the S&P 500. This is where the old saying, “Sell in May and Go Away” comes from. Despite the increased volatility, the S&P 500 managed to make it through on a positive note, with the S&P 500 up 1.7%. For the year so far, the S&P 500 has been up a whopping 20.55%, far exceeding what most experts were calling for this year. With the markets up so much already this year, you may wonder, “Will they run out of steam?”. A slowing economy and the trade war with China hold the potential to derail or boost returns on any given day, depending on how negotiations are going.

Interest rates

The clear winner for the quarter was bonds, as the increased volatility in U.S. equities sent investors into a more secure investment strategy, boosting the Bloomberg Barclays US Aggregate Bond Index 2.27%. So far for the year, this index is up 8.52% as the Federal Reserve has completely reversed course from tightening monetary policy (raising interest rates) to loosening monetary policy (lowering interest rates).

Interest rate activity was at the forefront of the headlines for the quarter, especially in September. During the month, eight of the top 10 developed market central banks met to discuss interest rates. The ECB (European Central Bank) and the Federal Reserve here in the U.S. were the only two to reduce target policy rates, but several others are discussing rate cuts in the months ahead. Meanwhile, here in the U.S., policymakers are projecting a third rate cut this year. We believe this will be very dependent on developments in trade talks with China, market returns, as well as the growth outlook globally and here in the U.S.

Meanwhile, a large portion of the world’s sovereign debt has negative yields making our treasury rates still very attractive to buyers overseas. This also is pressuring rates downward. As markets have continued to climb, we have been rebalancing here and increasing duration within bonds to offset market volatility more strongly (higher duration bonds tend to perform more positively than short duration bonds during a stock market retreat).

International Equities

International markets have lagged U.S. markets again during this quarter. The MSCI EAFE Index was down 1.07% while year to date is up 12.8%. So, the disparity between international and U.S. returns continued to grow during the quarter. Much of this is due to stronger economic growth in the U.S. versus overseas. Brexit, trade wars, and a strong U.S. dollar also continue to plague international returns.

Indicators

Our economic indicators continue to soften. While slightly above half are still looking positive, a few are flashing red, and positive indicators continue to become less positive or grow at a slower rate. The manufacturing index is one area teetering on the brink of contraction, giving the lowest reading in 10 years, but technically still giving a positive signal. Here are some others:

Impeachment

The House of Representatives is once again gearing up to attempt impeachment proceedings. Impeachment is the process whereby the House of Representatives, through a simple majority vote, brings charges against a government official. After the government official is impeached, the process then moves to the Senate to try the accused. The Senate must pass its vote by a two-thirds majority. (Note: Republicans hold 53 seats, while Democrats hold 47.) If this happened, President Trump would be removed from the office, and the Vice President would take his place.

There is little in recent history to help us understand how markets would react here in the U.S. if this were to happen. Bill Clinton was impeached in 1998, and Richard Nixon resigned during his Impeachment proceedings, but was never actually impeached. Several unsuccessful attempts have been made to impeach Donald Trump, George W. Bush, and, yes, even Barack Obama. When Bill Clinton was impeached, markets were down in bear market territory (over 20% peak to trough on the S&P 500) for a short time before they rallied back. The Russian Ruble Crisis also occurred at the same time, so it is hard to say whether the impact to markets was solely due to the impeachment process.

While removal of the President seems unlikely, short-term volatility would probably occur during any period of uncertainty. This is one of the many reasons we maintain a diversified portfolio. If stocks retreat, our bond portfolios would likely perform well, and international investments may strengthen in the face of a weaker dollar. A diversified portfolio, with cash or cash equivalents set aside for short-term needs, is the most effective solution to an extremely rare event like this.

Federal Debt

We are often asked about this topic; it seems to be an ever-present concern. While attending a conference in late September, I listened to Blackstone’s Byron Wien, a 60-year veteran of the markets. He put some very long-term perspective around the Federal debt levels and interest rates. He has been hearing “we can’t pass this along to our grandchildren” for the entire 60 years he has been in the business. He won’t go so far as to say the ratio of debt to GDP doesn’t matter, but believes we must put it into perspective.

According to Byron, today, the combined debt of the U.S is $22 trillion, up almost four times from 20 years ago, when it stood at about $6 trillion. However, the blended interest rate the government pays to service this debt is only up about 25% over what the government paid 20 years ago. It now costs $430 billion annually to service debt at current interest rates. This blends out to be just a bit over 2%; whereas, 20 years ago, it cost about $360 billion to service debt at a blended interest rate of a little over 6%. In summary, it is only 25% more costly to service our debt than it was 20 years ago, even though the amount of debt has quadrupled. Wien said these low-interest rates are “an economic gift from God.”

Are you curious about how your asset allocation looks? Are you using our new client portal? Did you know this is a secure way to move documents back and forth and that our contact information is at your fingertips? If you are already using the portal and want a primer on how to navigate or a link to login, check out the new instructional video on our website’s Client Login page. If you aren’t using the login, and you are interested, please reach out so we can send you the link to activate it!

On behalf of everyone here at The Center, we hope you enjoy the end of the year and the many holidays to come!

Angela Palacios CFP®, AIF®

Partner

Director of Investments

Angela Palacios, CFP®, AIF®, is a partner and Director of Investments at Center for Financial Planning, Inc.® She chairs The Center Investment Committee and pens a quarterly Investment Commentary.

Source of return data: Morningstar Direct The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Any opinions are those of Angela Palacios and not necessarily those of Raymond James. Expressions of opinion are as of this date and are subject to change without notice. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Investing involves risk and you may incur a profit or loss regardless of strategy selected. Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs or other fees, which will affect actual investment performance. Individual investor's results will vary. Past performance does not guarantee future results. Future investment performance cannot be guaranteed, investment yields will fluctuate with market conditions. The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. stock market.