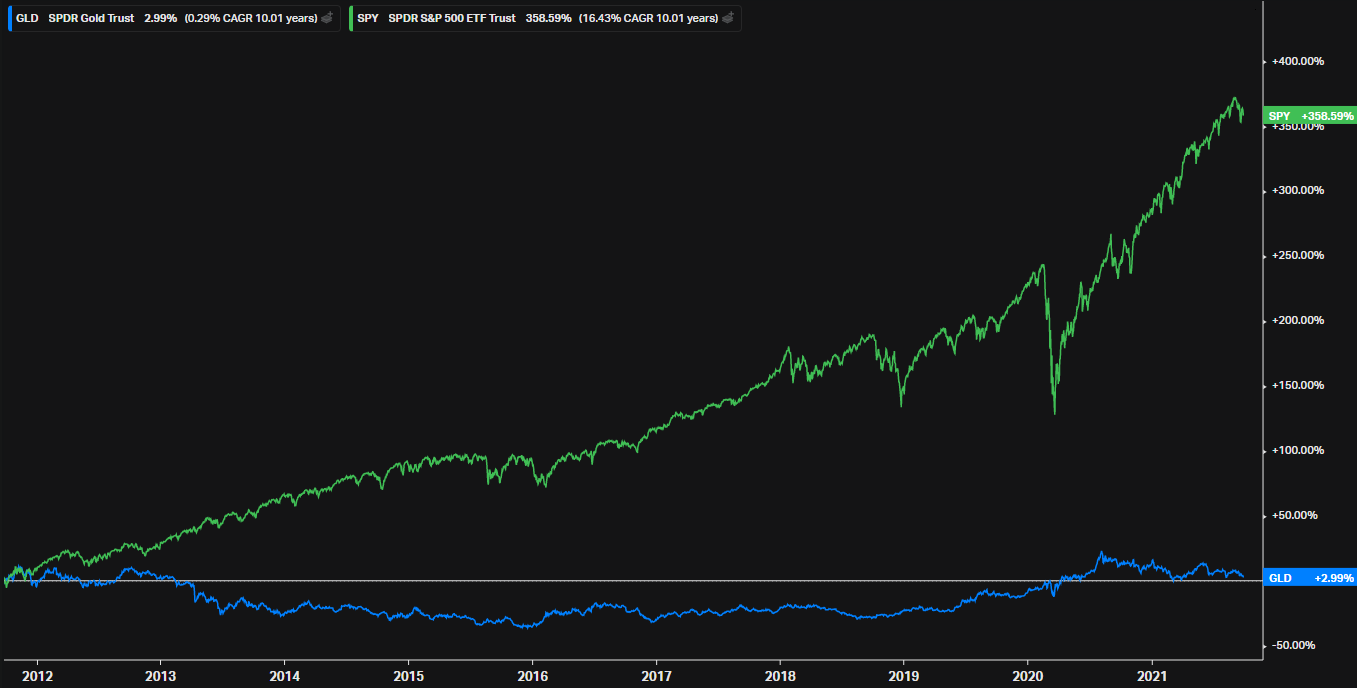

While it's easy to confuse positive stock market returns with economic growth, they are quite different. We can see this in the context of employment. Thirty-four percent of the S&P 500’s growth in 2020 can be attributed to technology, yet the technology sector only represents 2% of the US labor market. On the other hand, government, agriculture and other services, which is almost 40% of the labor market, is not even represented in the S&P 500. Concisely put, US stock strength doesn’t necessarily represent strength in the economy.

Digging into unemployment numbers, the unemployment rate decreased slightly to 6.7% in November. Nonfarm payrolls increased by 245,000 during the same month. Note, this is the weakest pace of payroll increases since the start of the recovery, which reflects a larger challenge. While 56% of the jobs lost between February and April have come back, only about 7% of that comeback has happened since September. We’re witnessing how hard it has been to have business and job growth while maintaining measures created to prevent the spread of covid-19. Both are important, so future job growth is dependent on how we negotiate the two moving forward.

Finally, let’s talk about inflation. Headline CPI and core CPI rose 0.2% month on month in November. Year on year, headline CPI was 1.2% and core CPI was 1.6%. Headline and core personal consumption expenditures (PCE) were generally flat, at 1.1% and 1.4% year on year, respectively. Due to low energy prices and economic slack, inflation ended lower in 2020 than in 2019. However, 2021 may be a different story. With a vaccine-facilitated boost to economic activity, prices hit hardest by the pandemic (think sporting events, dining, concerts, hotel rates, airfare, rent) could strengthen. We’ll likely see depressed prices start to go up. Many suspect the Federal Reserve will recognize this inflation is based on temporary factors, and will not raise interest rates to compress it. We are keeping an eye on how things play out. Overall, 2021 could foster a low and rising inflation environment.

Other investment headlines: Tesla & Bitcoin

You may have noticed two headlines gaining a lot of attention in the 4th quarter from two of the most volatile investments seen in 2020: Tesla and Bitcoin. Tesla finally recorded its fourth consecutive profitable quarter in a row which prompted its entry into the S&P 500. This means that if you own any fund that tracks the index, you now own a piece of TSLA! Albeit a small piece, as it makes up about 1.5% of the index.

Bitcoin was also back making headlines as it broke past its previous high from late 2017 and rose above $28k per BTC by the end of the year. Is the digital currency a speculative asset with no value or the world currency of the future? That is yet to be decided, but as it currently stood at year-end its market cap was ~540B – about the same market cap as Berkshire Hathaway.

COVID-19

The COVID-19 pandemic took a turn for the worse during the 4th quarter of 2020. Cases, hospitalizations, and deaths all continued to climb, but December brought us a glimmer of hope as the FDA expedited the approval process for two vaccines to be distributed across the country. Governor Whitmer gave guidance for the prioritization in Michigan, and the first phase began in December with health care workers who have direct exposure to the virus receiving round 1 of the 2-round vaccine. All essential frontline workers will follow, starting first with those aged 75 and older, then ages 65-74 and adults ages 16-64 with underlying medical conditions, finishing up with the rest of adults aged 16 and over. Click here for more details. We hope that these vaccines are a light at the end of the tunnel, and wish you all health and happiness going into the New Year.

Government Update

The $900 billion fiscal stimulus act continued to face headwinds in the final hour as President Trump changed his stance on the support to families. He called for an increase to the prior negotiated $600 stimulus payments to $2,000. The House narrowly voted in favor of this package and the change, only to be met by resistance in the Republican-led Senate. Voting on this was delayed resulting in $600 stimulus payments getting issued.

The package includes new funding for:

Restrictions placed on the Federal Reserve

The Federal Reserve (Fed) found itself amid the political battle of the stimulus package. It looks like the Fed may have to discontinue at the end of 2020 and potentially not be able to restart programs under the same terms that were backed by CARES Act funding, including:

Fed Chair Powell stated that these lending programs can still be restarted using Treasury’s Exchange Stabilization Fund but the effort to restrict this particular aspect of the Fed’s lending authority can be viewed as Congress stepping in and exerting oversight powers to limit how far the Fed can go in support of critical market functions. We will be watching the evolution of this debate and if the Fed’s communications become more restrained as a result. In the future, we may not be able to expect the Federal Reserve to step in and start buying secondary market issues to support prices.

The new Biden Administration

The run-off election held on January 5th in Georgia determined who holds the Senate. Democrats needed to win both of the Senate seats in Georgia to split the Senate 50-50. This meant that the democrat Vice President would be the tie-breaking vote giving a slight edge to the Democrats. This was the last major hurdle in understanding the makeup of the government for the next couple of years. This democratic advantage paves the way for a more ambitious President Biden legislative agenda. See our post-election update webinar for a summary of potential agenda items for the Biden administration. A shortlist includes President-Elect Biden’s proposed tax increases on corporations, income for those in the highest tax bracket, capital gains and estate taxes, aggressive health care changes, and the Green New Deal. While markets and the economy may favor party splits between the Presidency and Congress, an all-Democratic situation has still yielded positive outcomes for markets. The below chart shows that 27% of the time the Democrats have been in control and GDP growth has been at its best during these times and returns have been good as well.

Contributed by: Nicholas Boguth, CFA®

Contributed by: Nicholas Boguth, CFA®