Contributed by: Center Investment Department

Contributed by: Center Investment Department

Most delicious meals start with a great recipe. A recipe tells you which ingredients to use — and how much of each — to create something satisfying. In the same way, successful investing begins with understanding the right mix of assets that can help you reach your goals and stay comfortable along the way. Just as tastes and ingredients change or are tweaked over time, markets are ever evolving, so what has worked in the past may need periodic adjustments and thoughtful updates.

Determining the Right Mix

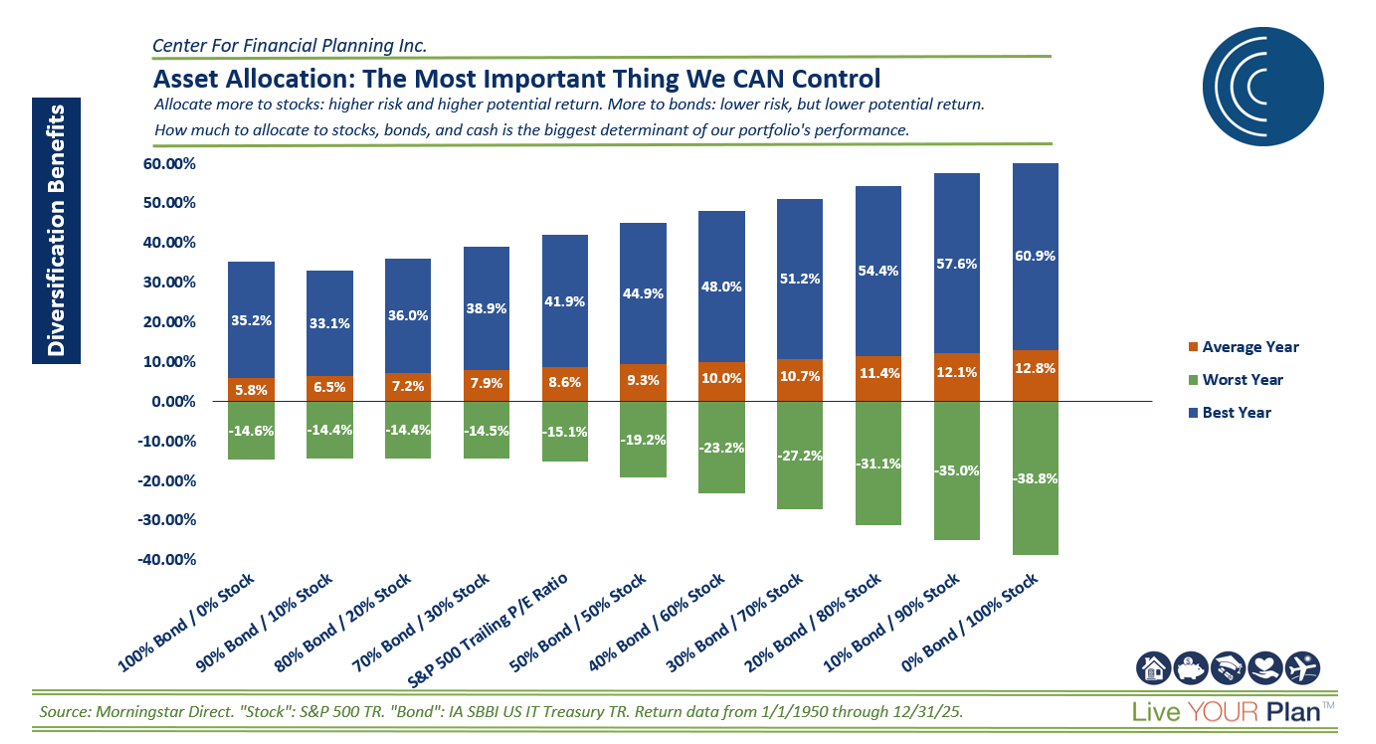

Asset allocation remains one of the most important drivers of long‑term investment outcomes and one of the few things investors can influence. It’s the foundational blend of stocks, bonds, and cash that shapes how your portfolio behaves, so choosing the right mix matters. This concept is perfectly depicted in the chart below, created by my colleague, Nick Boguth, CFA®, CFP®. This chart illustrates different asset allocation mixes and how they have historically produced varying ranges of outcomes. Portfolios with higher stock allocations have experienced higher best‑year returns but also greater drawdowns in worst‑year periods, while more conservative allocations (those with higher bond allocations) have shown narrower return ranges. This really highlights the trade‑off between risk and return that investors should consider when constructing a portfolio.

Now, choosing that mix may look different today than it did several years ago—it’s not static. And it might look different again in the future. To determine what will work best for you, start by answering three core questions:

What are my financial goals?

When do I need to achieve them?

How much will I be investing now — and over time — to support those goals?

Seasoning to Taste: Understanding Your Risk Tolerance

Even the perfect recipe can fall flat if it doesn’t match your palate. The same is true with investing. Imagine the equity market falls 20%. Would you feel tempted to sell stocks and flee to bonds or cash? Whether we like it or not, volatility has become a constant feature of today’s market environment, driven by changes in inflation, Federal Reserve policy shifts, and global uncertainty. We need to take these factors along with others, into consideration, and this is where risk tolerance comes into play. Understanding your comfort level with volatility and loss helps you select an allocation you can stick with, especially during challenging periods. When evaluating your tolerance, consider the risks and rewards associated with different investment types, how you react to market stress, how much loss you could tolerate for long term gains, and whether your emotions align with your strategy. Your feelings and behaviors matter just as much as the math.

Following the Recipe: Staying Disciplined

Just like sticking closely to a recipe produces more consistent results, staying committed to your asset allocation greatly increases your chances of long‑term success. But don’t get me wrong—it isn’t always easy!

Temptations to chase performance, react to alarming headlines, or invest in the “next big thing” are always present. Emotional responses to market swings, fear of missing out, and short‑term noise can all pull investors away from a thoughtfully designed plan, and often at exactly the wrong time. Over time, these small deviations can meaningfully change the risk and return profile of a portfolio. Several basic practices can help reinforce discipline and keep your plan on track:

Diversification: Spreading investments across asset classes and regions can help manage risk‑adjusted returns and potentially reduce reliance on any single outcome.

Regular Rebalancing: Periodically resetting your portfolio helps manage risk, maintain alignment with your goals, trim positions that have grown too large, and add to areas with future potential.

Dollar‑Cost Averaging: Investing consistently over time can help reduce the impact of market volatility and remove the pressure of timing decisions.

Bringing It All Together

We believe finding the right asset allocation is one of the most important steps in building a sound investment plan. By clarifying your goals, timeline, resources, and risk tolerance, you can create a mix that works for you.

Markets will continue to change, but the fundamentals don’t. Define your recipe, understand your palate, and follow the process with discipline. A consistent approach may help support long term investment objectives.

Securities offered through Raymond James Financial Services, Inc., member FINRA/SIPC. Investment advisory services are offered through Raymond James Financial Services Advisors, Inc.

Center for Financial Planning, Inc. is not a registered broker/dealer and is independent of Raymond James Financial Services.

This information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Any opinions are those of the author and are not necessarily those of RJFS or Raymond James. Every investor’s situation is unique and you should consider your investment goals, risk tolerance and time horizon before making any investment or investment decision. Investing involves risk, investors may incur a profit or loss regardless of strategy or strategies employed. Asset allocation does not ensure a profit or guarantee against a loss.

Dollar-cost averaging cannot guarantee a profit or protect against a loss, and you should consider your financial ability to continue purchases through periods of low price levels.