We just got to enjoy what has been called “The Greatest Two Minutes in Sports.” I have always been a fan of the Kentucky Derby, the horses, the outrageous hats, wondering who is wearing the hats, and a blanket of roses. I’ve had the privilege of actually going down to Louisville to watch but I have never been part of the glamorous, hat-wearing crowd. We’ve always watched from the infield, though “watch” is a loose term. It is more like standing on your tip toes to see a blur of horses run by you for about one-tenth of a second and then return to drinking your mint julep. But it is fun nonetheless.

We just got to enjoy what has been called “The Greatest Two Minutes in Sports.” I have always been a fan of the Kentucky Derby, the horses, the outrageous hats, wondering who is wearing the hats, and a blanket of roses. I’ve had the privilege of actually going down to Louisville to watch but I have never been part of the glamorous, hat-wearing crowd. We’ve always watched from the infield, though “watch” is a loose term. It is more like standing on your tip toes to see a blur of horses run by you for about one-tenth of a second and then return to drinking your mint julep. But it is fun nonetheless.

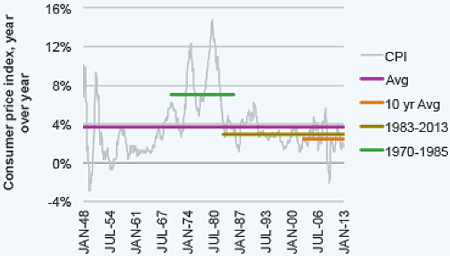

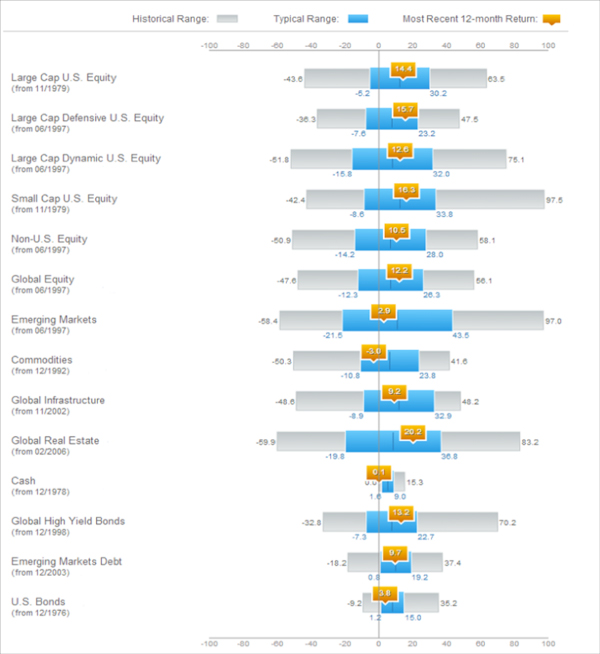

This year the market has felt a lot like we have been off to the races. It has been one of the strongest starts to the year this decade. Is it too much too fast? A new chart put out by Russell Investments says maybe not.

For additional disclosure and interpretive guidance on this chart, please click on the following link: http://www.russell.com/Helping-Advisors/Markets/acd.aspx?d=t

How to interpret the chart:

- The gray bar is the full range of 1 year returns the asset class has experienced throughout history

- The blue portion of the bar is where returns fall most of the time (68%)

- The number highlighted in orange is where returns fell for the 12 months that ended as of March 31st, 2013

Even with the strong returns, as of recently, most indexes are still hovering near “middle of the road” returns for the past 12 months. So perhaps it hasn’t been too much too quickly.

If you are seeking some advice on an appropriate strategy for your portfolio, put the odds in your favor and contact your Financial Planner today!

Angela Palacios, CFP®is the Portfolio Manager at Center for Financial Planning, Inc. Angela specializes in Investment and Macro economic research. She is a frequent contributor to Money Centered as well asinvestment updates at The Center.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website’s users and/or members.