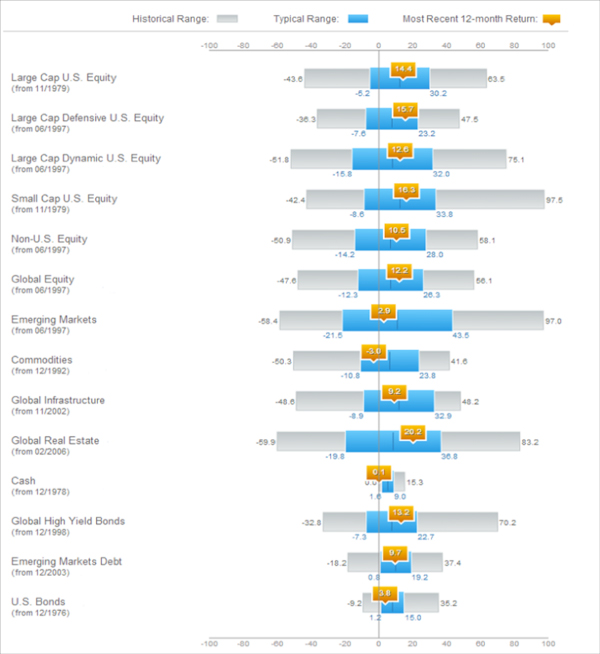

Most investors are familiar with the infamous “Black Monday” stock market crash. The Dow Jones Industrial Average (DJIA) dropped by a whopping 22.61% in one day on Monday October 19, 1987. Many may not be as familiar with records that are being set right now for Tuesdays. May 28th marked the 20th Tuesday in a row where the Dow Jones Industrial Average ended on an up note. This is a record breaking streak of gains for any specific day of the week in the history of the DJIA. The previous high count was 13 days in a row and has occurred on 3 separate occasions for Monday, Wednesday and Friday with the most recent streak occurring in 1900!

Most investors are familiar with the infamous “Black Monday” stock market crash. The Dow Jones Industrial Average (DJIA) dropped by a whopping 22.61% in one day on Monday October 19, 1987. Many may not be as familiar with records that are being set right now for Tuesdays. May 28th marked the 20th Tuesday in a row where the Dow Jones Industrial Average ended on an up note. This is a record breaking streak of gains for any specific day of the week in the history of the DJIA. The previous high count was 13 days in a row and has occurred on 3 separate occasions for Monday, Wednesday and Friday with the most recent streak occurring in 1900!

This Tuesday winning streak that began on January 15th has included 1,573 points for the Dow or 83% of the years gains for the index as of May 28th. The picture below is a total of Year to date points made or lost cumulatively on the particular day of the week for the DJIA.

http://buzz.money.cnn.com/2013/06/04/dow-tuesday-streak/

There has been much speculation as to why Tuesday has been so great?

Here are some of the arguments.

- The federal reserve is buying bonds through their open market operations on Tuesday and Friday’s

- Retail investors placing mutual fund buy orders on Monday, after looking at their accounts over the weekend, and then the managers are putting that money to work on Tuesday.

- Automated trading programs that seek out trends have noticed this trend and started to buy in anticipation, and as such, perpetuating the trend.

- Or it could just be random

While the debate of why this phenomenon has occurred may not be over, unfortunately, the winning streak itself is over as of Tuesday June 4th.

http://www.bespokeinvest.com/thinkbig/2013/5/28/20-for-tuesday.html

Angela Palacios, CFP®is the Portfolio Manager at Center for Financial Planning, Inc. Angela specializes in Investment and Macro economic research. She is a frequent contributor to Money Centered as well asinvestment updates at The Center.

The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. The Dow Jones Industrial Average (DJIA), commonly known as “The Dow” is an index representing 30 stock of companies maintained and reviewed by the editors of the Wall Street Journal. Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs or other fees, which will affect actual investment performance. Individual investor's results will vary. Past performance does not guarantee future results.