Contributed by: Center Investment Department

Contributed by: Center Investment Department

We at The Center know that people can be overwhelmed with difficult decisions, especially during stressful life events such as job loss or change.

GM recently announced plant closings and layoffs across the country, which will affect thousands of workers. This hits close to home for those of us in the Motor City and reminds us to look at your investment portfolio, ensure proper allocations, and ask these questions:

Am I close to retirement?

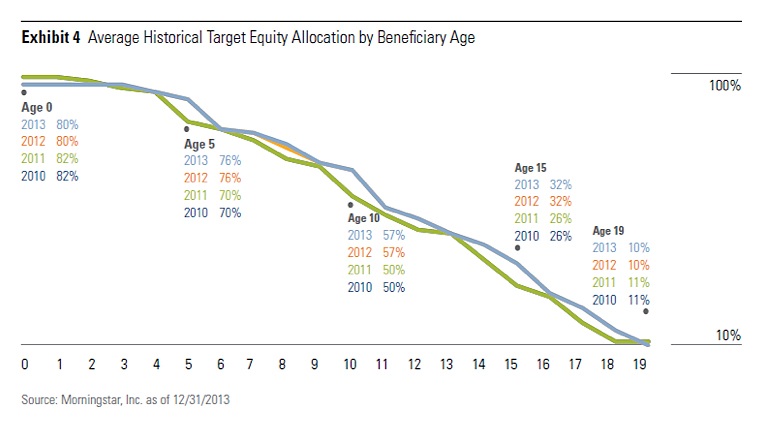

It may be time to scale back your portfolio’s risk. If you are invested within a target date retirement fund, this may already be happening for you.

How long before I have to use this money?

With funds you won't need for more than 5-10 years, you may want to ensure you are taking enough risk to help meet your goals. If you are invested within a target date retirement fund, this may already be happening for you.

What is my ability to take risk?

You may be able to take on more risk if you don't depend entirely on your portfolio. In this case, a target date fund may not be appropriate.

Do I get uneasy or worried when my portfolio drops by a certain percentage and feel the need to take action?

If this affects your decision making, even under normal circumstances, guidance from an advisor during a time of change may help alleviate additional stress.

What Can I do?

Review the investments in your account and your beneficiaries. We often neglect our 401(k) accounts in times of change.

Maintain a diversified portfolio to help stay on track for your retirement goals. Some plans offer an overwhelming number of choices, while other plan offerings seem insufficient to diversify a portfolio. Your advisor can help with your comprehensive investment strategy, especially during challenging times.

When you’ve spread assets among multiple financial institutions, maintaining an effective investment strategy – one that accurately reflects your goals, timing, and risk tolerance – may become difficult. Consolidate, and your financial professional can help ensure these assets are part of an overall allocation strategy that reflects your current financial situation and long-term retirement goals.

For more information on consolidating retirement accounts, read “Simplifying Your Retirement Plans.”

Any opinions are those of the author and not necessarily those of RJFS or Raymond James. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Expressions of opinion are as of this date and are subject to change without notice.

Every type of investment, including mutual funds, involves risk. Risk refers to the possibility that you will lose money (both principal and any earnings) or fail to make money on an investment. Changing market conditions can create fluctuations in the value of a mutual fund investment. In addition, there are fees and expenses associated with investing in mutual funds that do not usually occur when purchasing individual securities directly.